Assessee was entitled to deductions u/s 80JJAA and additional depreciation in Tamil

- Tamil Tax upate News

- March 11, 2025

- No Comment

- 52

- 75 minutes read

Robert Bosch Engineering and Business Solutions Pvt. Ltd. Vs DCIT (ITAT Bangalore)

Conclusion: An employee should be employed for 300 days or more during the previous year should be applied cumulatively across the year of hiring and the following year, rather than restricting it to the first year. The overall increase in employment exceeded 10% when using the correct interpretation and assessee was eligible for the deduction under Section 80JJAA. Further, computers used for software development were essential to the production process and should be classified as plant and machinery for depreciation purposes. Thus, both the 80JJAA deduction and additional depreciation was allowable.

Held: Assessee-company was engaged in software development, IT-enabled services, and embedded software development for automobile components. It had claimed a deduction of Rs.21.16 crore under Section 80JJAA for wages paid to new regular workmen and additional depreciation on computers used for software development. AO disallowed the 80JJAA deduction, stating that the company did not meet the requirement of increasing its workforce by at least 10% over the previous year, as required under the Act. AO also argued that only employees who completed 300 days of work in the year of hiring should be considered. AO concluded that the company failed to meet the threshold. CIT(A) upheld this view, leading the company to file an appeal before the ITAT. The questions arose for consideration was whether assessee qualified as an industrial undertaking, and whether the development of computer software and IT-enabled services amounted to the manufacture or production of an article or thing under Section 80JJAA, whether assessee was claiming double benefits by first availing exemptions under Sections 10A and 10AA and subsequently under Section 80JJAA, whether the condition that an employee should be employed for 300 days or more during the previous year must be met in the particular assessment year or cumulatively over two assessment years. It was held that Karnataka High Court judgment in Aquarelle India Ltd. vs. DCIT ruled that the 300-day requirement should be applied cumulatively across the year of hiring and the following year, rather than restricting it to the first year. It found that the overall increase in employment exceeded 10% when using the correct interpretation. Based on this finding, ITAT ruled that assessee was eligible for the deduction under Section 80JJAA. The company also claimed additional depreciation on computers used for software development, arguing that software development qualified as “production of an article or thing” under Section 32(1)(iia). AO disallowed the claim, stating that software was not a tangible article or thing and that computers did not qualify as plant and machinery. The software development required significant technical effort and qualified as production under various Supreme Court and High Court rulings. Tribunal also observed that computers used for software development were essential to the production process and should be classified as plant and machinery for depreciation purposes. Tribunal allowed both the 80JJAA deduction and additional depreciation, directing the AO to recompute the tax liability.

FULL TEXT OF THE ORDER OF ITAT BANGALORE

This is an appeal filed by the assessee against the order passed by the CIT(A) – 14, Bengaluru dated 28/02/2020 in ITA No.ITBA/APL/M/250/2019-20/1025986267(1) for the assessment year 2012-13.

2. Both the assessee and the revenue are in appeal.

First, we take up the appeal of the assessee in IT(TP)A No. 593/Bang/2020

3. The assessee, through a letter dated 17th March 2021, raised following additional/supplementary grounds of appeal:

“Additional/Supplementary Grounds of Appeal:

1. Having regard to the facts and circumstances in the instant case and having regarding to the provisions of law, the Appellant pleads the Hon’ble ITAT to direct the AO to grant relief by way of restricting the levy of the dividend distribution tax, on the dividend distributed/paid to Robert Bosch GmbH, Germany, to 10% in terms o f Article 10 of the DTAA between India and Germany, instead o f 16.2225% charged in terms of section 115-0 of the Act.

2. The Appellant pleads the Hon’ble ITAT to direct the AO to refund the excess Dividend Distribution Tax paid by the Appellant as per section 237 of the Act.

3. Whether on the facts and in the circumstances of the case and in law, the Education Cess and Higher and Secondary Education Cess, being cess on tax payable on Total Income under the provisions o f the Act other than section 115JB of the Act is allowable as a deduction?

4. The Appellant craves leave to add to, amend or alter the ground herein.

5. For these and other grounds that may be urged at the time o f hearing, the appellant prays for appropriate relief. ”

4. In the application filed for the admission of the additional ground, the assessee pleaded that the issues raised in the additional grounds of appeal are legal in nature and go to the root of the matter. Accordingly, the learned Authorised Representative (AR) for the assessee requested that these grounds be admitted for adjudication.

5. On the other hand, the learned Departmental Representative (DR) opposed admitting the additional grounds of appeal on the reasoning that they were not raised before the authorities below.

6. We have heard both the parties and perused the materials available on record. At the outset we note issue raised in additional ground of appeal is legal in nature having bearing on computation of correct income and the assessment framed. Furthermore, no new facts are required to be examined for adjudicating the additional grounds of appeal. Considering the legal nature of the issue and its necessity for computing the correct income in the assessment, and respectfully following the decision of the Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. vs. CIT (229 ITR 383), we hereby admit the additional ground of appeal.

6.1 The interconnected issue raised by the assessee through ground numbers 1 to 11 of its appeal is that the learned CIT(A) erred in confirming the disallowance of the deduction under Section 80JJAA of the Act. This includes the first-year claim of ₹12,55,83,331/- pertaining to the year under consideration and the second claim of ₹8,60,71,538/-pertaining to the assessment year 2011-12.

6.2 The facts in brief are that the assessee company, Bosch Global Software Technologies Pvt. Ltd. (formerly known as Robert Bosch Engineering and Business Solutions Pvt. Ltd.), is a wholly-owned subsidiary of Robert Bosch GmbH, Germany. The company is engaged in the business of developing computer software, providing IT-enabled services, and developing embedded software for automobile components and accessories.

6.3 In its return of income for the year under consideration, the assessee claimed a deduction under Section 80JJAA of the Act amounting to ₹21,16,54,868/- only. Out of this, ₹8,60,71,538/- pertains to the immediate previous assessment year (A.Y. 2011-12), while the remaining ₹12,55,83,331/- pertains to the year under consideration (A.Y. 2012-13).

6.4 The Assessing Officer (AO) observed that the deduction under Section 80JJAA of the Act is allowed for additional wages paid to new regular workmen employed by an assessee company deriving income or profit from an industrial undertaking engaged in the manufacture or production of articles or things. According to clause (i) of the Explanation to Section 80JJAA(2) of the Act, “additional wages” refers to wages paid to new regular workmen employed during the previous year, provided the number of such workmen is not less than 10% of the existing employees as on the last day of the preceding year. Furthermore, clause (ii)(c) of the Explanation specifies that “regular workmen” are those who have completed at least 300 days of employment in the previous year. Based on this legal framework, the AO found that the number of new regular workmen employed by the assessee during the year who completed 300 days stood at 320 only, whereas the total number of existing workmen on 1st April 2011 was 3,582 only. Therefore, the condition of a 10% increase in the number of employees was not fulfilled. Similarly, in the immediate previous assessment year (A.Y. 2011-12), the assessee employed 160 new workmen who completed 300 days, which was also less than 10% of the existing workmen as on 1st April 2010. Consequently, the AO concluded that the conditions for claiming a deduction under Section 80JJAA were not met. Hence, the AO disallowed the deduction claim of ₹21,16,54,868/- and made a corresponding addition to the total income of the assessee.

7. The aggrieved assessee preferred an appeal before the learned CIT(A).

8. The assessee, before the learned CIT(A), submitted that during the year, it had employed a total of 1,606 employees, while 82 employees resigned during the same period. Hence, the net addition to employment during the year was 1,524, which is significantly more than 10% of the existing employees (3,582) as on the last date of the preceding assessment year. The assessee contended that the AO had erroneously considered only those employees hired on or before 6th June of the relevant year to comply with the condition under clause (ii)(c) of the Explanation to Section 80JJAA(2) of the Act, which requires workmen to be employed for at least 300 days during the previous year.

8.1 The assessee argued that the condition precedent is that new workmen should be employed for 300 days or more, not that the workmen should complete 300 days of work within the relevant previous year. The assessee also clarified that in the business, there are two types of workmen: fixed-term employees and permanent employees. The 300-days requirement, it argued, applies only to fixed-term employees, as permanent employees are hired with the intent of continuous employment until retirement, making the condition irrelevant to them.

8.2 Without prejudice to the above argument, the assessee further stated that a deduction of ₹3,79,44,492/- had already been allowed for A.Y. 2011-12 as the first-year claim. Therefore, the AO could not disallow the same claim for the second year (A.Y. 2012-13).

8.3 However, after considering the facts, the learned CIT(A) upheld the AO’s disallowance. The ld. CIT(A) held that the requirement of employing new regular workmen for 300 days or more in the previous year is mandatory. Relying on the order of the Tribunal in the case of Texas Instruments (India) Pvt. Ltd. (ITA No. 703/Bang/2016), the ld. CIT(A) concluded that the net increase in employees fulfilling the 300-day condition was less than 10%, and therefore, the assessee was not eligible for the deduction under Section 80JJAA of the Act.

8.4 Additionally, the ld. CIT(A) observed that the appellant assessee had claimed exemptions under Sections 10A and 10AA of the Act for its two SEZ units, namely Coimbatore CHIL and Coimbatore TIDEL Park. Referring to Section 80A(4) of the Act, the ld. CIT(A) opined that no further deduction under Section 80JJAA could be allowed for units whose profits were already claimed as exempt under Sections 10A or 10AA of the Act. Consequently, the ld. CIT(A) disallowed the claim for these units.

8.5 The ld. CIT(A) further disallowed the deduction under Section 80JJAA of the Act on the grounds that the provision applies only to assessee deriving profits from industrial undertakings engaged in the manufacture or production of articles or things. The ld. CIT(A) held that the appellant assessee, engaged in software development and IT-enabled services, did not meet this requirement.

9. Being aggrieved by the order of the learned CIT(A), the assessee is in appeal before us.

10. The learned AR before us filed a paper book running from pages 1 to 750, written submission having 13 pages, a chart explaining the transfer pricing issues having 11 pages, various case laws along with its compilation and contended that the number of employees employed in the year in dispute is far exceeding 10% of the employees as on the last day of the previous year. The ld. AR in support of his contention filed the auditors certificate place on pages 524 – 525 of the paper book. As per the ld. AR it is not necessary that the number of employees should complete 300 days in the previous year in which they were employed. As such the continuity of their services should be seen which may overlap more than a year. The ld. AR further submitted that the deduction claimed in the earlier year cannot be denied in the year under consideration. Similarly, the ld. AR also argued that the assessee has not claimed any deduction under section 80JJAA of the Act for the units eligible for exemption under section 10A/AA of the Act. It was also argued that the activity of software development tantamount to manufacturing and therefore the assessee cannot be denied the benefit of deduction under section 80JJAA of the Act.

11. On the other hand, the learned DR vehemently supported the order of the authorities below.

12. We have heard the rival contentions of both parties and perused the materials available on record. The facts of the case at hand have been elaborately discussed in the preceding paragraphs, which are not in dispute. Hence, we are not inclined to repeat the same for the sake of brevity. Based on the preceding discussion, we note that the following questions arise for our adjudication:

1. Whether the assessee qualifies as an industrial undertaking, and whether the development of computer software and IT-enabled services amounts to the manufacture or production of an article or thing under Section 80JJAA of the Act.

2. Whether the appellant assessee is claiming double benefits by first availing exemptions under Sections 10A and 10AA of the Act and subsequently under Section 80JJAA of the Act.

3. Whether the condition that an employee should be employed for 300 days or more during the previous year must be met in the particular assessment year or cumulatively over two assessment years.

12.1 The provisions of section 80JJAA of the Act provide deduction in respect of wages paid to new workman. The precondition to apply the provision of section 80JJAA of the Act is that the total income of the assessee being Indian company includes income from industrial undertaking which is engaged in manufacture or production or article or things. The term industrial undertaking has not been defined for the purposes of section 80JJAA of the Act. However, the same has been defined for the purpose of provision of section 10(15) of the Act which reads as under:

Explanation 1.—For the purposes of this sub-clause, the expression i”ndustrial undertaking” means any undertaking which is engaged in—

(a) the manufacture or processing of goods; or

(aa) the manufacture of computer software or recording of programme on any

disc, tape, perforated media or other information device; or

(b) the business of generation or distribution of electricity or any other form of power; or

(ba) the business of providing telecommunication services; or

(c) mining; or

(d) the construction of ships; or

(da) the business of ship-breaking; or

(e) the operation of ships or aircrafts or construction or operation of rai l systems.

12.2 The above definition includes the manufacture of computer software as an industrial undertaking. Since the term “industrial undertaking” is not specifically defined for the purposes of Section 80JJAA of the Act or any other relevant provisions of the Act, we are inclined to rely on the definition provided under Section 10(15) of the Act. The appellant assessee is engaged in the development of computer software, IT-enabled services, and the development of embedded software for automobile components and accessories, which, in our considered opinion, falls within the definition of an industrial undertaking.

13. The next connected issue arises whether the activity of the assessee can be described as manufacture or production of article or thing. The term manufacture has been defined under the Act by inserting the provision of section 2(29BA) of the Act through the Finance Act 2009, however the term production has not been defined. The provision of section 2(29BA) of the Act defines the term manufacture as under:

(29BA) “manufacture”, with its grammatical variations, means a change in a non-living physical object or article or thing,—

(a) resulting in transformation of the object or article or thing into a new and distinct object or article or thing having a different name, character and use; or

(b) bringing into existence of a new and distinct object or article or thing with a different chemical composition or integral structure;

14. From the above definition, it is clear that for an activity to qualify as “manufacture,” it must involve a change in a non-living physical object that results in a completely new and distinct object with a different name, character, and use. In our understanding, the process of computer software development does not involve a non-living physical object or article. Therefore, the assessee’s activity of developing software or embedded software for automobile components and accessories may not apparently qualify as the “manufacture” of an article or thing.

14.1 However, it is important to note that the provisions of Section 80JJAA of the Act use the term “manufacture or production.” This distinction implies that “production” is broader than “manufacture,” and an industrial undertaking may qualify for the deduction if it engages in either manufacturing or production activities.

14.2 The term “production” refers to the process of creating goods and services by combining various resources such as labor, capital, raw materials, and technology. It encompasses a wide range of activities. The Oxford English Dictionary defines “production” as “that which is produced; a thing that results from any action, process, or effort; a product of human activity or effort.”

14.3 The Hon’ble Supreme Court, in the case of CIT vs. N.C. Budharaja & Co. (204 ITR 412), observed that the term “production” is broader than the term “manufacture.” The relevant observations of the Hon’ble Supreme Court are as follows:

The word ‘production’ or ‘produce’ when used in juxtaposition with the word ‘manufacture’ takes in bringing into existence new goods by a process which may or may not amount to manufacture. It also takes in all the byproducts, intermediate products and residual products which emerge in the course o f manufacture of goods.

14.4 The development of computer software involves intellectual and technical efforts to create a product or service with economic value, thereby fulfilling the criteria for production. Inputs such as human expertise, technology, and tools (e.g., coding platforms) are combined to produce software, aligning with the general definition of production. The output, typically intangible (a software application or code), is a hallmark of production in knowledge-based or service-oriented industries. Therefore, in our considered opinion, the activity of the assessee amounts to the production of an article or thing.

14.5 Before concluding, it is important to note that in the immediately preceding assessment year, the assessee had also claimed a deduction under Section 80JJAA of the Act. This claim was disallowed due to a dispute regarding the requisite number of employees not completing 300 days of employment in the previous year. However, no questions were raised regarding the nature of the assessee’s business. This indicates that, in the preceding assessment year, the revenue authorities had accepted the assessee as an industrial undertaking engaged in the manufacture or production of an article or thing.

14.6 Based on the above observations, the finding of the learned CIT(A) that the assessee company is not an industrial undertaking engaged in manufacture or production does not hold merit. Accordingly, we set aside the finding of the learned CIT(A) on this matter. Hence, the first question is answered in favor of the assessee.

15. The next question is whether the assessee is claiming a double benefit by availing exemptions under Sections 10A and 10AA of the Act, as well as a deduction under Section 80JJAA of the Act. Admittedly, the assessee company has two units: the Coimbatore CHIL unit and the Coimbatore TIDEL Park unit, whose profits or gains are claimed as exempt under the provisions of Sections 10A and 10AA of the Act. The learned CIT(A) observed that, pursuant to the provisions of Section 80A(4) of the Act, double benefits cannot be allowed to the assessee for the same income under different provisions of the Act.

15.1 In this context, we note that the learned AR for the assessee submitted before us that no deduction under Section 80JJAA of the Act was claimed in respect of wages paid to the employee of Coimbatore CHIL unit and the Coimbatore TIDEL Park unit. However, we find that this claim has not been verified by the lower authorities.

15.2 For the sake of justice and fair play, we are inclined to set aside this issue to the file of the Assessing Officer (AO) for verification. The AO is directed to examine the claim of the learned AR and decide the issue accordingly. The assessee is also directed to provide all necessary details to substantiate that no deduction was claimed under Section 80JJAA of the Act for wages paid to employees of the two units eligible for exemptions under Sections 10A and 10AA of the Act.

15.3 Coming to the third question, regarding the requirement of 300 days of employment, we note that this issue has already been adjudicated by the Tribunal in the assessee’s own case for the immediately preceding assessment year, i.e., A.Y. 2011-12, in IT(TP)A No. 608/Bang/2016. In its order dated 02-02-2022, the Tribunal held as under:

We have perused the submissions advanced by both sides in light of records placed before us. On bare reading of section 80JJ AA of the Act, following requirements emerges to be fulfilled in order to claim deduction under the section:

1. The Assessee should be an Indian Company and the gross total income of the Assessee should include profits and gains derived from any industrial undertaking engaged in the manufacture or production of article or thing. Admittedly this condition is satisfied in the case of the Assessee.

2. There are certain prohibition laid down in Sec. 80JJAA(2) of the Act and it is not the case of the Ld.AO that these prohibitions are applicable in the case of the Assessee.

3. The new workmen employed must be a regular workmen and the number of such new workmen employed should be in excess of one hundred workmen employed during the previous year.

4. The increase in the number of regular workmen employed during the year should not be less than ten per cent of existing number of workmen employed in such undertaking as on the last day of the preceding year;

5. If the above conditions are satisfied then 30% of the additional wages paid to new regular workmen employed by the assessee in the previous year, shall be allowed as deduction for three assessment years including the assessment year relevant to the previous year in which such employment is provided.

Therefore, if some workmen were employed for a period of less than 300 days in the previous year then no deduction is allowable in respect of payment o f wages to such work men in the present year even if such workmen was employed in the preceding year for more than 300 days but in the present year, such workmen was not employed for 300 days or more. By the very same reasoning the fact that in the first year of employment the additional wages paid is not allowed deduction for the reason that the workmen did not work for 300 days or more but if the next two Assessment years, if he works for more than 300 days each, then the deduction u/s.80JJAA of the Act has to be allowed. It is not proper to say that if the deduction is refused in the first year of employment of the new employee then for the next two succeeding Assessment Years also, the benefit of deduction will not be available. Such an approach defeats the very purpose for which deduction u/s.80JJAA of the Act is allowed for three consecutive Assessment years. This aspect has now been clarified in the finance Act, 2018 by adding a second proviso to the definition of additional employee in Explanation (ii) to Sec.80JJAA of the Act. Even prior to such curative or clarificatory amendment, we are of the view that the claim for deduction u/s.80JJAA of the Act ought not have been disallowed. The Ld.AO is therefore directed to verify the details and consider the claim o f assessee in accordance with law.

Accordingly, this ground raised by assessee stands remanded to the Ld.AO for due verification.

15.4 We note that the Tribunal, in the aforementioned order, directed that if an employee does not complete 300 days of employment in the previous year relevant to the assessment year under consideration, then the wages paid in respect of such an employee will not be eligible for deduction. However, if the employee completes 300 days of employment in the subsequent assessment year, the wages paid to such an employee in the subsequent two years will become eligible for deduction. With these directions, the Tribunal set aside the issue to the file of the Assessing Officer (AO).

15.5 At the time of the hearing before us in the matter of the current assessment year, the learned AR of the assessee referred to a recent judgment of the Hon’ble Karnataka High Court in the case of Aquarelle India Ltd. vs. DCIT (157 taxmann.com 244). In this judgment, the Hon’ble High Court observed that the requirement of 300 days of employment should be considered cumulatively across both the previous year and the succeeding year. As such, for availing the benefit under Section 80JJAA of the Act, it is not mandatory for the workmen to have worked for 300 days in a single previous year. The relevant observation of the Hon’ble High Court reads as under:

12. After considering the aspect of working for 300 days in the previous year, this Court in Texas Instruments has held that period of 300 days could be taken into consideration both in the previous and succeeding years for the purpose of availing the benefit under section 80JJAA of the Act and it is not required that workmen works for 300 days in the previous year relevant to assessment year.

15.6 The order of the Tribunal in the assessee’s own case for A.Y. 2011-12, as discussed above, was passed without considering the judgment of the Hon’ble High Court (immediate above), as the same was not available on record at that time. Therefore, in light of the recent judgment of the Hon’ble High Court, we are inclined to depart from the earlier stand taken by the Tribunal in the assessee’s own case and hold that the requirement of 300 days of employment should be considered cumulatively across both the previous year and the succeeding year. Hence, the third question is hereby decided in favour of the assessee.

15.7 Based on the detailed examination of the facts and the relevant legal provisions, we set aside the findings of the learned CIT(A) and direct the Assessing Officer to consider the matter in line with the above observations. Hence the ground of appeal of the assessee is hereby partly allowed for statistical purposes.

16. The next issue raised by the assessee, as per grounds 12 to 14 of its appeal, is that the learned CIT(A) erred in confirming the disallowance of the claim for additional depreciation under Section 32(1)(iia) of the Act.

17. The assessee, in its return of income, claimed additional depreciation under section 32(1)(iia) of the Act on computers used for the production of software. The assessee explained that it was in the business of software development, which amounts to the production of an article or thing, and that the computers used for software production qualify as plant and machinery, thus making them eligible for additional depreciation.

17.1 On the other hand, the AO held that computer software is not an article or thing. The AO noted that while the term “article or thing” is not defined under the Act, an inference can be drawn from the provisions of Section 10A of the Act, where the phrase “export of articles or things or computer software” is used meaning thereby the computer software is different from article or things. The AO concluded that computer software is distinct from an article or thing, and additional depreciation is allowable only on plant and machinery installed by an assessee engaged in the manufacture or production of articles or things.

Further, the AO observed that computers and computer software are depreciated at higher rates than plant and machinery, which suggests that computers are not considered plant and machinery. Consequently, the AO disallowed the claim and made an addition of Rs. 13,73,17,444 only.

18. Aggrieved, the assessee, preferred an appeal before the learned CIT(A), reiterating that it was engaged in the business of developing embedded software for automobile components and accessories. The production/development of such software requires significant effort, processes, and human involvement, and therefore, should be considered as the business of “manufacture or production of articles or things.” The assessee placed reliance on the order of the Tribunal in the case of Manhattan Associates (India) Development Centre (112 taxmann.com 200) and the judgment of the Hon’ble Supreme Court in the case of Chrestien Mica Industries Ltd. vs. State of Bihar [1961] 12 STC 150.

18.1 The assessee also cited the judgment of the Hon’ble Karnataka High Court in CIT vs. Datacons Pvt. Ltd. (21 taxman 341), and the Hon’ble Delhi High Court in CIT vs. Radio Today Broadcasting Ltd. (64 taxmann.com 164).

18.2 Additionally, the assessee referred to the definition of “activity of article or thing or operation” under the 14th Schedule of the Act, which includes “electronics, including computer hardware and software, and information technology-related industries.”

18.3 Further, the assessee submitted that the Income Tax Rules classify fixed assets into four categories: Building, Furniture & Fixtures, Plant & Machinery, and Ships. Plant & Machinery is further subdivided into different classes, each subject to different depreciation rates. Computers and computer software are included in the plant & machinery category and depreciated at higher rates. Therefore, the fact that computers and computer software are depreciated at a higher rate does not mean that they are not considered plant & machinery.

18.4 However, the learned CIT(A) confirmed the disallowances made by the AO by observing as under:

“As seen from the above, a plain reading of the provisions shows that new machinery or plant should be acquired and installed by an assessee who is engaged in the business of manufacture or production of any article or thing. The assessee is not engaged in manufacture/production of article or thing but in provision of software services. The assessee has not demonstrated with evidence that it is manufacturing or producing any products which are identifiable. As seen from the annual report and website of the company, assessee provide various services to its customers in different domains. AS per the financial statements of the assessee the revenue is from software services only. Even as per the segmental reporting forming part o f the annual report the assessee reported to be engaged exclusively into services segment. This clearly shows that the assessee is not into manufacture or production of article or thing but into providing services and solutions to the customer.

The contention of the assessee that the software development activity carried out resulted in generation of a new product which is intangible can not be accepted. What assessee offers is\ service and the revenue is generated through that source. The assessee has not provided any evidence with regard to production of any product/article/thing. The scope of operations of the assessee can not be expanded artificially expanded to include services. Supreme court constitutional bench) in the case of Dilip Kumar &Co (95 Taxman.com 327) held that tax exemptions/clauses/provisions have to be read strictly and in case of ambiguity it must be interpreted in favour o f revenue. Considering the above the contentions of the assessee with regard to production of product is rejected.

The legislative intent is very clear to provide the incentive for specified industries producing article or thing in factory/business premises using plant/machinery. That is the reason why plant/machinery installed office/residential premises are not made eligible. In sections like 10A/10AA/10B etc, specific mention is made for computer services so as to allow deduction for assesses engaged in IT sector. Non-inclusion of computer services or other services clearly shows the legislative intent not to include them in the amobit of sec.32. The case laws mentioned by the assessee do not cover the facts of the case. In the case of CIT vs. Oracle software India (2010-T1OL-04-SC-IT), The Court in the context of sec.801A stated that producing new compact discs with loaded content constitutes manufacture/process. It is pertinent to note that appellant is not engaged in any such manufacture/process. It is also interesting to note the observations of Hon’ble Supreme Court in the very same case which held that “Where the issue arises for determination, the department should study actual process undertaken by the assessee to decide whether there is manufacture or processing”. In the context of present case, it factually observed that no manufacture or similar eligible process is undertaken by the assessee. Accordingly the assessee is not eligible for the above claim.

The other cases quoted by the assessee are either factually distinguishable or relate to some other section. In case of Datacons, the assessee was engaged in processing some basic data in the form of cash vouchers, invoices, indents etc., by using computers and converting it into a suitable format for the final statements. The court held this activity as processing of goods and accordingly held the company as industrial company. In the case of Radio Today Broadcasting Ltd, the Delhi High Court concurred with the view of the ITAT that production of radio programmes involves the technica l processes of recording, editing, copying and then broadcasting and that amounting and that amounted to production of an article or thing and therefore, the assessee was eligible for additional depreciation. In the case of Peerless Consultancy Services, the Calcutta High Court relied on Datcons case law and held the assessee therein, engaged in the activity of electronic data processing, as an industrial company for the purposes of investmet allowance. The Calcutta High Court, in the case of Show Wallace & Co, once again relied on the optacons case law and held that business carried on by that assessee in its computer division with the aid of computer systems was industrial undertaking which satisfied the conditions contained in section 32A(2)(b)(iii). The Kerala High Court relied on this decision of Calcutta High Court i.e., Shaw Wallace case and held in the case of computerized accounting and management services (supra) that the assessee who was doing business in computerized accounting and management services by using computers is an industrial undertaking for the purpose of section 32A. Also Shaw Wallace case quoted by the assessee relates to investment allowance and Statronics case relates to the location of Plant/machinery whether in office premises or not. ln all these cases, the decisions o f the courts are based on a concurrent finding that there was processing of goods in as much as the inputs and amounts to manufacturing or production of article or thing as envisaged in provisions relating to investment allowance. Probably, in the backdrop of these decision, a definition of ‘manufacture’ came to be inserted in the Act in section 2(29BA) through Finance Act, 2009. These decisions cannot be applied to the appellant’s case, as there are no inputs nor there was any processing of goods. In fact the appellant offered software development as a service and had shown revenue there from in the account. In so far as section 32(1)(iia) is concerned, it covers the assesses who are engaged in manufacture or production of article or thing only. Provision of services for development o f software has been kept out of purview of section 32(1)(iia). Therefore, assessee providing software development services is not eligible for additional depreciation.

For the detailed discussion above, it is held that software/IT services provided by the assessee do not constitute manufacture/production of article or thing and hence assessee is not eligible for additional depreciation u/s 32(1)(iia) of the Act. All the grounds raised by the assessee are accordingly rejected on this issue and disallowance o f AO sustained. Hence, the Ground No. 6, 7 & 8 are dismissed.

19. Being aggrieved by the order of the learned CIT(A), the assessee is in appeal before us.

19.1 The learned AR before us reiterated the arguments by contending that the activity of software development is a manufacturing activity and therefore the assessee is entitled for the additional depreciation claimed under sections 32(iia) of the Act.

20. On the other hand, the learned DR before us vehemently reiterated the findings contained in the order of the authorities below.

21. We have heard the rival contentions of both the parties and perused the materials available on record. Admittedly the assessee has claimed additional depreciation under clause (iia) of section 32 of the Act by treating the computers used for development of computer software as plant and machinery installed for manufacture or production of article or things. The claim of the assessee has disallowed by the lower authorities by holding the assessee’s business of computer software development & IT enabled services does not tantamount to manufacture or production of article or things. Further, the computers on which additional depreciation was claimed does not qualify as plant and machinery.

21.1 As per far as the question, whether the assessee is in the business of manufacture or production of article or things is concern. We note that same has been answered by the us in the preceding paragraph while dealing the with the ground of appeal in respect of claim of deduction under section 80JJAA of the Act. As previously noted, the assessee is engaged in the business of developing of computer software, and embedded software for automobile components and accessories, which involves the application of intellectual and technical efforts, and meets the criteria for the production of an article or thing. In line with this, the assessee’s business activities fall under the broader definition of “production” under the Act, and thus, the development of software constitutes a form of production in a knowledge-based industry.

21.3 The argument that computers used in the development of software are part of plant and machinery is substantiated by the fact that the Income Tax Rules categorize computers and computer software within the block of plant and machinery, eligible for depreciation at a higher rate. This indicates that computers software, despite being intangible in terms of output, play a crucial role as plant and machinery in the production process.

21.4 Given that the assessee is engaged in the production of an article or thing (software), the computers used in the production of such software can be treated as plant and machinery under the provisions of Section 32(1)(iia) of the Act. Therefore, the claim for additional depreciation on the computers used in the production of software is in line with the provisions of the Act.

21.5 In light of the above, we hereby reverse the findings of the learned CIT(A) and allow the assessee’s claim for additional depreciation under Section 32(1)(iia) of the Act.

22. The next issue raised by the assessee vide ground No. 15 is that the learned CIT(A) erred in confirming the disallowances of maintenance charges for Rs. 27,71,000/- by treating prior period item.

23. The AO found that the “repair & maintenance charges others” includes an amount of Rs. 27.71 Lakh paid to Coimbatore Hitech Infrastructure Pvt Ltd as maintenance charges at the rate of Rs. 1 Lakh per annum per acer for the period 1st April 2010 to 31st March 2011 and debit note issue by the party in this respect as on 21st January 2011. Thus, the same relates to previous years not to the year under consideration but the same was claimed in the year under consideration. Hence the AO disallowed the same by holding that the prior period item as well as expenses incurred were not wholly and exclusively for business purposes.

24. On appeal by the assessee, the learned CIT(A) confirmed the disallowance made by the AO by observing as under:

“5.5.1 The assessee contended before the AO that the expenditure got crystallized only during the current year and therefore the expenditure is allowable in the current year. The same arguments are repeated before the appellate forum also. The contentions o f the assessee are carefully considered. The AO clearly brought on record the debit notes pertaining to the earlier period. The fact that debit notes are raised prior to the F.Y shows that the agreement for services and actual rendering of services happened during the prior period. Hence, such expenditure can not be debited in the current year. The profits of each year need to be determined separately. Hence, the arguments put forth by the assessee are rejected and addition sustained. Hence, Grounds 11 & 12 are dismissed. ”

25. Being aggrieved by the order of ld. CIT-A, the assessee is in appeal before us.

26. The learned AR before us contended that the impugned expenses were crystalised in the under consideration which can be verified from the debit note placed on page 587 of the paper book dated 12th of September 2011. Thus, as per the Ld. AR, the deduction such prior period expenses should be allowed while computing the taxable income of the assessee.

27. On the other hand, the learned DR vehemently supported the order of the authorities below.

28. We have heard the rival contentions of both the parties and perused the materials available on record. Prior period expenses are those expenses that relate to an earlier accounting period but are recognized or incurred in the current financial year. These expenses could be related to the previous year’s business, and are often found when errors are discovered or when payments are made after the relevant accounting period. The provisions of Section 37(1) of the Income Tax Act allow the deductions for any expenditure (not being capital expenditure or personal expenditure) that is incurred wholly and exclusively for the purposes of business or profession. Prior period expenses are generally deductible under this provision, provided they meet the following conditions:

-

- The Expense Must Relate to the Business: It must be a legitimate business expense incurred in the prior period that is subsequently recognized in the current period.

- Accrual Basis of Accounting: The expense should have been incurred in the prior period under the accrual accounting method but recognized and paid in the current period.

- Adjustment in Books: The accounting treatment of prior period expenses should be appropriately reflected in the books of account for the current period. For instance, adjustments for such expenses should be made through prior period adjustments in the financial statements.

- Disclosure Requirements: The prior period expenses should be separately disclosed in the financial statements of the current year, clearly stating the period to which they relate.

28.1 When a prior period expense is allowed as a deduction under Section 37(1), it directly reduces the taxable income for the current period. The expense is typically deducted in the year in which it is crystalized, even though it pertains to a previous period. In holding so we draw support and guidance from the judgment of hon’ble Calcutta High Court in case of PCIT vs. Balmer Lawrie and Company Ltd reported in 149 taxmann.com 286 where in it was held as under:

It is noted that the Commissioner (Appeals) has taken specific note of the fact that the expenses claimed by the assessee as prior period, the liability to pay had crystallized during the relevant previous year and therefore the claim was allowed. Further the Tribunal noted that no appeal was preferred by the revenue against the orders of the Commissioner (Appeals) for the assessment years 2007-08 to 2009-10 and the appeals filed by the revenue for the assessment years 2010-11 and 2011-12 were dismissed by the Tribunal. Further the Tribunal has pointed out that the revenue was unable to bring any material or fact to disprove the assessee’s explanation furnished before the authorities in support of its claim that liability to pay expenses charged under the head ‘priorperiod’ crystallizedduring the financial year 2011-12. Further on perusing the details furnished by the assessee with regard to those expenses, the Tribunal noted that the assessee had claimed deduction in respect of items which were revenue in nature and therefore fully allowable in arriving at its business income. Further, the Tribunal has pointed out that the revenue did not controvert the contention raised by the assessee that no deduction in respect of these expenses was allowed in the prioryears and the tax rate in the earlier years and in the year under consideration were same and therefore irrespective of the year of deduction allowed, the revenue’s effect was taxed neutral. The Tribunal also referred to the decision of the High Court of Gujarat in Pr. CIT v. Adani Enterprises Ltd. [Tax Appeal No. 566 of 2016, dated 20-072016] and found the said decision to be relevant to the facts and circumstances of the case. Thus, it is found that the Commissioner (Appeals) and the Tribunal has examined the facts and granted relief to the assessee and more importantly that for the earlier assessment yearsi.e. 2005-06, 2009-10, the revenue has accepted the orders passed by the Commissioner (Appeals). Though the appeal was filed before the Tribunal for the assessment years 2010-11 and 2011-12, the same were dismissed. Thus, a consistent view is required to be adopted in the absence of any material placed by the revenue before the required Tribunal to show that there was any distinguishing feature in the assessment year under consideration to make a departure from the earlier view. [Para 4]

28.2 Now turning to the facts of the present case, we note that the debit note was raised by the party dated 12 September 2011 for the impugned expenses pertaining to the period from 1st April 2010 to 31 March 2011 which is placed on page 587 of the paper book. Thus, it is transpired that the liability to expenses in dispute were crystalised in the year under consideration and therefore the same was claimed as deduction in the current year.

28.3 The 2nd controversy arises whether such expenses were incurred for the purpose of the business and the same were not capital in nature. In this regard, we note that the maintenance charges were paid for the maintenance of the property. There is no information available on record whether such property was purchased by the assessee as investment or for the purpose of the business. In the absence of such information, we are inclined to remit the issue to the file of the AO for fresh adjudication as per the provisions of law after considering the discussion stated above. Hence the ground of appeal of the assessee is hereby partly allowed for statistical purposes.

29. The next issue raised by the assessee, vide ground Nos. 16 to 18 of its appeal is that the learned CIT(A) erred in confirming the disallowance made u/s 14A of the Act for ₹33,39,350/- only.

30. During the year, the assessee earned exempt income of ₹5,14,05,256/- and made a suo moto disallowance of expenses under Section 14A of the Act, amounting to ₹11,54,264/- only. The assessee explained that this self-determined disallowance was made after identifying expenses directly related to the exempt income. Therefore, it contended that the provisions of Rule 8D of the Income Tax Rules were not applicable.

30.1 However, the Assessing Officer (AO) disagreed with the assessee’s contention. The AO calculated the disallowance as per Rule 8D and determined the amount to be ₹33,39,350/- only. Accordingly, the AO made an additional disallowance over and above the suo moto amount disallowed by the assessee.

31. On appeal by the assessee, the learned CIT(A) confirmed the addition made by the AO.

32. Being aggrieved by the order of the learned CIT(A), the assessee is in appeal before us.

33. The learned AR before us submitted that the assessee has already made suo Moto disallowance under the provisions of section 14A of the act which has not been disputed by the authorities below. Therefore, the provisions of rule 8D of Income Tax Rules cannot be invoked automatically by the revenue unless the disallowance made by the assessee is rejected based on cogent reasons.

34. On the other hand, the learned DR before us vehemently supported the order of the authorities below.

35. We have heard the rival contentions of both the parties and perused the materials available on record. At the outset, we note that that issue of disallowance under section 14A of the Act is covered in favour of the assessee by the order of this Tribunal in own case of the assessee for A.Y. 2010-11 bearing IT(TP)A No. 608/Bang/2016 dated 02-12-2022. The relevant finding of the Tribunal is extracted as under:

The Ld. Counsel submitted that assessee had disallowed Rs.2,23,20,919/-against exempt income earned being Rs.3,63,96,471/- u/s. 14A of the Act. He submitted that during the year under consideration, the investments made by assessee were only fixed. He submitted that assessee is not into buying and selling of shares / investments but is carrying on software development businesses. The Ld. Counsel submitted that assessee has computed disallowance at Rs. 36,01,783/- as under:

***********

12. The Ld. Counsel submitted that the entire investments cannot be taken into consideration for disallowance under Rule 8D(2)(iii) at 0.5%. The Ld. DR on the contrary relied on the orders passed by the authorities below. We note that on identical issue, the Coordinate Bench of this Tribunal in assessee’s own case observed for Assessment Year 2008-09(supra) as under:

“9.1 We heard the parties on this issue. The Ld A.R invited our attention to page 521 of the paper book, wherein the details of investments are given. He submitted that the assessee has made investments only in units of various mutual funds. The aggregate amount of investments made during this year was Rs.90.59 crores. He further submitted the assessee has also invested a sum of Rs.15.00 crores in growth scheme and a sum of Rs.20.26 crores in dividend reinvestment scheme. The assessee has made investments in six schemes only during the year under consideration and it has encashed investments made in the earlier years in four schemes. He submitted that the assessee has not really incurred any expenditure in earning the dividend income. On the contrary, the Ld D.R supported the order passed by Ld CIT(A). 9.2 We heard the parties on this issue and perused the record. We notice that opening balance of investments stood at Rs.25.59 crores in four schemes of mutual funds. During the year under consideration, the above investments have been realised. The assessee has made fresh investments in six schemes of mutua l funds during this year, out of which three schemes fall under Growth/reinvestment schemes. Considering the less number of schemes, in our view, it may not be proper to apply Rule 8D mechanically. Accordingly, we are of the view that the disallowance may be estimated to meet the requirements of sec.14A of the Act. Accordingly, we estimate the disallowance u/s 14A at Rs.2.00 lakhs and in our view, the same would meet the requirements of the provisions of sec.14A of the Act. Accordingly, we set aside the order passed by Ld CIT(A) on this issue and direct the AO to restrict the disallowance u/s 14A to Rs.2.00 lakhs. ”

13. In the above observations for Assessment Year 2008-09, there no disallowance was made by assessee this Tribunal deem it appropriate to restrict the disallowance to Rs.2 Lakhs considering the less number of schemes that fall under growth / investment schemes. Going by the above principle and also observing the fact that the Ld.AO has not expressly mentioned any dissatisfaction in the suomoto disallowance computed by assessee we hold that the disallowance computed by the assessee is appropriate.

35.1 Before us, no material has been placed on record by the Revenue demonstrating that the decision of the Tribunal in the own case of the assessee as discussed above has been set aside/stayed or overruled by the Higher Judicial Authorities. Before us, no material was placed on record pointing out any distinguishing feature in the facts of the case of earlier AY and the year under consideration. Thus, respectfully following the order of the Tribunal in the own case of the assessee as discussed above, we hereby set aside the finding of the learned CIT(A) and direct the AO to delete the disallowance made by him. Hence, the ground of appeal of the assessee is hereby allowed.

36. The next issue raised by the assessee is that the learned CIT-A

erred in considering certain comparables while calculating the ALP of the international transaction carried out by the assessee with its associated enterprise.

37. The necessary facts are that the assessee company, during the year, is engaged in various types of international transactions with associated enterprises. For transfer pricing purposes, the assessee categorized these transactions into two distinct segments: the Software Development Segment and the ITES Segment.

37.1 Under the Software Development Segment, the assessee reported operating revenue of ₹1,600,47,03,775/- and operating costs of ₹1,374,06,84,618/-, resulting in an Operating Profit to Operating Cost (OP/OC) ratio of 16.48% only.

37.2 Similarly, under the ITES Segment, the assessee reported operating revenue of ₹132,28,05,755/- and operating costs of ₹117,12,02,386/-, leading to an OP/OC ratio of 12.94% only.

38.3 In the Transfer Pricing (TP) study, the assessee adopted the Transactional Net Margin Method (TNMM) as the most appropriate method and used the Operating Profit to Operating Cost (OP/OC) ratio as the Profit Level Indicator (PLI). The assessee selected a different set of comparables for both segments and determined the PLI of comparable companies by considering the weighted average margin of three years’ data. The assessee calculated the PLI of the comparable companies at 17.59% for the Software Development Segment and 12% for the ITES Segment, and accordingly, claimed that both segments were at Arm’s Length Price (ALP) only.

38.4 The Transfer Pricing Officer (TPO), after analysing the TP study report, accepted the Software Development Segment as being at ALP. However, the TPO rejected the assessee’s TP analysis for the ITES Segment. The TPO disqualified the comparable companies selected by the assessee, citing the following reasons:

i. The use of non-current year data.

ii. Improper application of the export turnover filter.

iii. Improper application of the employees cost filter.

38.5 Subsequently, the TPO conducted a fresh search for comparable companies using the following filters:

– Companies not having current year data were excluded.

– Companies with incomes of less than ₹1 crore were excluded.

– Companies with revenue from ITES or software development (SWD) less than 75% of total turnover were excluded.

– Companies with export turnover less than 75% of total turnover were excluded.

– Companies with RPT of more than 25% of sales were excluded.

– Companies with an employee cost of less than 25% of turnover

-were excluded

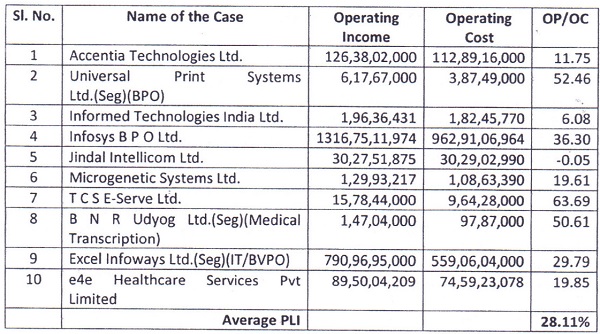

38.6 Based on these filters, the TPO selected a set of 10 comparable companies. Using single-year data, the TPO calculated the PLI of the comparable companies at 28.11%. The list of comparable companies and the detailed working of the PLI by the TPO are as follows:

38.7 The TPO further made an adjustment on account of working capital and recalculated the arm’s length margin for OP/OC at 28.48%, as compared to the margin declared by the assessee at 12.94%. Consequently, the TPO determined an upward adjustment of ₹18,19,55,070/- only.

39. The aggrieved assessee filed an appeal before the CIT(A), and among other contentions, objected to the comparability of the new set of comparable companies selected by the TPO.

40. The learned CIT(A), after considering the facts in totality, held that out of the 10 comparable companies selected by the TPO, 2 companies viz, Universal Print Systems Ltd and BNR Udhyod Limited failed the service revenue filter. Consequently, these two companies were excluded by the learned CIT(A) from the set of comparables. Accordingly, the CIT(A) confirmed the comparability of the remaining 8 companies selected by the TPO.

41. Pursuant to the order of the learned CIT(A), the ALP margin was recalculated at 90%, as against 28.48% computed by the TPO. Subsequently, the assessee filed a rectification request before the learned CIT(A), highlighting an error in the computation of the margin of one comparable company, namely Microgenetic Systems Ltd. The rectification was accepted by the CIT(A), and the revised ALP margin was determined at 21.27% of OP/OC.

42. Being aggrieved by the order of the learned CIT(A), both the assessee and the Revenue have filed appeals before us. The assessee is in appeal against the admission of certain companies as comparable whereas the revenue is in appeal against the exclusion of 2. comparables. The relevant ground of appeal of the Revenue in IT(TP)A No. 446/Bang/2020 reads as under:

“4. The Learned CIT(A) and the AO erred in holding that `New Employees’ (who are recruited on permanent basis) who have joined after 4th June of AY 2011-12 and AY 2012-13 and who have worked for less 300 days of the respective years do not fall within the meaning of ‘Regular Workmen ‘and accordingly erred in not considering them as `New Regular Workmen’. ”

42.1 The learned AR before us reiterated that certain companies should not be considered as comparable as their turnover exceeds the limit of 200 crores. Likewise, the learned AR contended that the TPO has made certain calculation error in respect of a company, E4e Healthcare Services Ltd. by treating the bank cost as non-operating expenses. As such it was argued by the learned AR the bank charges should be treated as operating cost while calculating the margin of the comparable company.

42.3 The learned AR further submitted that the company namely Excel Infoways Ltd. does not meet the filter criteria adopted by the TPO and therefore the same should not be considered.

On the other hand, the learned DR before us reiterated the findings contained in the order of the authorities below.

43. Both the ld. AR and the DR before us vehemently supported the order of the authorities below as favourable to them.

44. We have heard the rival contentions of both parties and perused the materials available on record. It is an admitted fact that the assessee’s TP study for the ITES Segment was rejected by the TPO, who conducted fresh benchmarking after selecting a new set of comparable companies. On subsequent appeal, the learned CIT(A) partly allowed the appeal of the assessee by excluding certain companies selected by the TPO on the grounds of failing comparability criteria.

44.1 The first issue for our consideration is whether companies with a turnover exceeding ₹200 crores should be excluded when calculating the ALP for the assessee, given the fact that the assessee’s turnover under the ITES Segment is only ₹132.28 crores. In this context, it is relevant to refer to the order of the Tribunal in the case of Autodesk India Private Limited, reported in 96 taxmann.com 263, wherein it was held as follows:

17.7 We have considered the rival submissions. The substantial question o f law (Question No.1 to 3) which was framed by the Hon’ble Delhi High Court in the case of Chryscapital Investment Advisors (India) Pvt. Ltd., (supra) was as to whether comparable can be rejected on the ground that they have exceptionally high profit margins or fluctuation profit margins, as compared to the Assessee in transfer pricing analysis. Therefore as rightly submitted by the learned counsel for the Assessee the observations of the Hon’ble High Court, in so far as it refers to turnover, were in the nature of obiter dictum. Judicial discipline requires that the Tribunal should follow the decision of a non-jurisdiction High Court, even though the said decision is o f a non-jurisdictional High Court. We however find that the Hon’ble Bombay High Court in the case of Pentair Water India (P.) Ltd. (supra) has taken the view that turnover is a relevant criterion for choosing companies as comparable companies in determination of ALP in transfer pricing cases. There is no decision of the jurisdictional High Court on this issue. In the circumstances, following the principle that where two views are available on an issue, the view favourable to the Assessee has to be adopted, we respectfully follow the view of the Hon’ble Bombay High Court on the issue. Respectfully following the aforesaid decision, we uphold the order of the DRP excluding 5 companies from the list of comparable companies chosen by the TPO on the basis that the 5 companies turnover was much higher compared to that the Assessee.

17.8 In view of the above conclusion, there may not be any necessity to examine as to whether the decision rendered in the case of Genisys Integrating Systems (I) (P.) Ltd. (supra) by the ITAT Bangalore Bench should continue to be followed. Since arguments were advanced on the correctness of the decisions rendered by the ITAT Mumbai and Bangalore Benches taking a view contrary to that taken in the case of Genisys Integrating Systems (I) (P.) Ltd. (supra), we proceed to examine the said issue also. On this issue, the first aspect which we notice is that the decision rendered in the case of Genisys Integrating Systems (I) (P.) Ltd. (supra) was the earliest decision rendered on the issue of comparability o f companies on the basis of turnover in Transfer Pricing cases. The decision was rendered as early as 5.8.2011. The decisions rendered by the ITAT Mumbai Benches cited by the learned DR before us in the case of Willis Processing Services (supra) and Capegemini India (P.) Ltd. (supra) are to be regarded as per incurium as these decisions ignore a binding co-ordinate bench decision. In this regard the decisions referred to by the learned counsel for the Assessee supports the plea of the learned counsel for the Assessee. The decisions rendered in the case of NTT Data (supra), Societe Generale Global Solutions (supra) and LSI Technologies (supra) were rendered later in point of time. Those decisions follow the ratio laid down in Willis Processing Services (supra) and have to be regarded as per incurium. These three decisions also place reliance on the decision of the Hon’ble Delhi High Court in the case of Chriscapital Investment (supra). We have already held that the decision rendered in the case of Chriscapital Investment (supra) is obiter dicta and that the ratio decidendi laid down by the Hon’ble Bombay High Court in the case of Pentair (supra) which is favourable to the Assessee has to be followed. Therefore, the decisions cited by the learned DR before us cannot be the basis to hold that high turnover is not relevant criteria for deciding on comparability of companies in determination of ALP under the Transfer Pricing regulations under the Act. For the reasons given above, we uphold the order of the CIT(A) on the issue of application of turnover filter and his action in excluding companies by following the ratio laid down in the case of Genisys Integrating (supra).

44.2 Based on the above findings of the ITAT, we are inclined to exclude companies with a turnover exceeding ₹200 crores as comparables while calculating the ALP for the international transactions carried out by the assessee with its Associated Enterprise (AE). According to the assessee, the list of companies with a turnover exceeding ₹200 crores is as follows:

(i) Infosys BPO Limited

(ii) TCS E-Services Ltd

44.3 Hence, we direct the TPO/AO to exclude the companies listed above from the set of comparables while calculating the ALP for the international transactions carried out by the assessee, provided they have a turnover exceeding ₹200 crores. This exclusion shall be made after conducting the necessary verification.

44.4 The next comparable company selected by the TPO and confirmed by the learned CIT(A), which has been objected to by the learned AR of the assessee, is Excel Infoways Ltd. According to the learned AR, the impugned company fails both the employee cost filter and the service revenue filter.

44.5 The learned AR pointed out that the employee cost of the company is 13.05%, which is below the threshold limit of 25% as applied by the TPO. Similarly, the service revenue of the company is 51.06%, which falls short of the required threshold of 75% under the respective filter applied by the TPO. In this regard we note that the based on the filters applied by the TPO, it is evident that the impugned company fails to meet the employee cost filter (13.05% against the threshold of 25%) and the service revenue filter (51.06% against the threshold of 75%). These deviations from the prescribed criteria render the company unsuitable as a comparable.

44.6 However, since the above details require factual verification, we deem it appropriate to remand the matter to the file of the AO/TPO for necessary verification. The AO/TPO is directed to re-examine the compliance of Excel Infoways Ltd. with the filters applied, and if the company is found to fail the thresholds, it shall be excluded from the list of comparables for the purpose of determining the ALP.

46.7 The next contention raised by the learned AR pertains to the inclusion of Cameo Corporate Services Ltd. as a comparable. According to the learned AR, the company was excluded from the set of comparables by the TPO on the ground that its current year data was not available in the public domain at the time of assessment. However, we find that the current year data was available before the ld. CIT-A as evident from the finding of the ld. CIT-A in his order but the same was not accepted. The learned AR has submitted that the current year data is available and has further argued that the functions performed by the impugned company are identical to those of the assessee.

46.8 In light of the above submission, we find merit in the argument of the learned AR that exclusion on account of non-availability of data is no longer valid if the requisite data is now accessible. However, since the functional similarity and other comparability criteria require verification, we remand the matter to the AO/TPO for necessary verification. If, upon examination, the functions of Cameo Corporate Services Ltd. are found to be similar to those of the assessee, and the company satisfies the required filters, it shall be included in the list of comparables for determining the ALP.

46.9 The next contention raised by the learned AR relates to an error in the computation of the margin of the comparable company, E4e Healthcare Services Ltd. The learned AR has pointed out that the TPO, while computing the margin, erroneously treated bank charges as a non-operating cost, which has impacted the margin calculation.

46.10 We find merit in the argument of the learned AR, as bank charges are generally considered an operating expense in the context of transfer pricing analysis. However, this issue requires factual verification to determine whether the treatment of bank charges as non-operating cost was indeed an error.

46.11 Accordingly, we remand this issue to the file of the AO/TPO for necessary verification. The AO/TPO is directed to re-examine the treatment of bank charges in the computation of the margin for E4e Healthcare Services Ltd. and, if found erroneous, make the necessary correction.

46.12 Regarding the inclusion of 5 comparable companies by the revenue namely M/s Accentia Technological Ltd., Informed Technologies India Ltd., Jindal Intellicom Ltd., Micro-genetic system Ltd., and e4e healthcare services private limited, the learned AR appearing on behalf of the assessee did not raise any objection. Accordingly, we sustain the inclusion of such companies in the list of comparables while calculating the ALP of the assessee with respect to the international transactions carried out by it. Hence, the ground of appeal of the assessee, is partly allowed for statistical purposes.

47. Coming to ground of appeal raised by the revenue against the exclusion of comparable companies namely Universal Print System Ltd and BNR Udhyog Limited, we note that the ld. CIT-A has given categorical finding that these 2 companies do not meet the criteria adopted by the AO /TPO for selecting the comparables. As such these 2 companies do not meet the criteria of 75% for revenue from the operations of ITeS services. This finding of the ld. CIT-A has not been disputed by the learned DR appearing on behalf of the revenue. Accordingly, we do not find any reason to interfere in the finding of the learned CIT-A. Hence, the ground of appeal of the revenue is hereby dismissed.

47.1 The first issue raised by the assessee through additional ground of appeal is that it has paid the corporate dividend tax at a rate higher than the rate specified under DTAA. Accordingly, the learned AR before us contended that the assessee should be granted the refund of excess corporate dividend tax paid by it. The learned AR further submitted that in this regard, a direction can be issued to the AO for necessary adjudication as per the provisions of law. On the other hand, the ld. DR did not raise any serious objection if the issue is set aside to the file of the AO for necessary verification and fresh adjudication as per the provisions of law. After hearing both the parties, in the interest of justice and fair play, we direct the AO to charge the tax on the dividend declared by the assessee in pursuance to the provisions of the Act. Accordingly, we set aside the issue to the file of the AO for fresh adjudication as per the provisions of law. Hence the additional ground raised by the assessee is allowed for statistical purposes.

47.2 The assessee in the 2nd additional ground of appeal requested to allow the deduction for the education cess, and higher and secondary education cess while computing the income under normal computation. The assessee in the additional ground of appeal has claimed the deduction of the cess paid on the income tax on the reasoning that same is revenue expenditure. However, we note that there is an amendment under the provisions of section 40(a)(ii) of the Act by the Finance Act 2022 wherein an explanation has been inserted with retrospective effect i.e. assessment year 2005-06. The amendment reads under:

[Explanation 3.—For the removal of doubts, it is hereby clarified that for the purposes of this sub-clause, the term “tax” shall include and shall be deemed to have always included any surcharge or cess, by whatever name called, on such tax;]

47.3 As per the above amendment, there remains no ambiguity to the fact that the assessee cannot claim the deduction of the cess by treating the same as revenue expenditure. Thus, we do not find any merit in the additional ground of appeal raised by the assessee. Hence, the ground of appeal raised by the assessee is hereby dismissed.

48. In the result, the appeal of the assessee is partly allowed for statistical purposes.

Coming to the ITA No. 446/Bang/2020, an appeal by the revenue

49. The first issue raised by the Revenue is that the learned CIT(A) erred in allowing the claim for the provision of doubtful debts amounting to ₹22,98,957/- only.

50. The AO observed that the assessee had debited a sum of ₹22,98,957/- to its profit and loss account as a provision for doubtful debts. According to the AO, this amount represents a contingent liability and, therefore, it is not allowable as an expense. Consequently, the AO disallowed the provision and added it to the total income of the assessee.

51. The aggrieved assessee filed an appeal before the learned CIT(A) and argued that the issue is covered by the decision of the Hon’ble Supreme Court in the case of Vijaya Bank v. CIT (190 Taxman 257), and the decision of the Hon’ble Karnataka High Court in the case of Sadvik Asia (S.T.R.P No. 76/2016, dated 29-06-2018). The learned CIT(A) agreed with the submissions of the assessee and deleted the disallowance made by the AO.

52. Being aggrieved by the order of the learned CIT(A) the revenue is in appeal before us.

53. Both the ld. DR and the AR before us vehemently supported the order of the authorities below as favourable to them.

54. We have heard the rival submissions of both the parties and perused the materials on record. The learned CIT(A) has categorically held that the issue under consideration is identical to the decisions of the Hon’ble Supreme Court in the case of Vijaya Bank v. CIT (190 Taxman 257) and the Hon’ble Karnataka High Court in Sadvik Asia (S.T.R.P No. 76/2016, dated 29-06-2018). The ld. DR for the Revenue has not brought any contrary facts or judicial precedents on record to dispute the applicability of these decisions to the facts of the case. In the absence of such contrary evidence, and in light of the binding precedents of the Hon’ble Supreme Court and the High Court, we find no reason to interfere with the findings of the learned CIT(A). Hence the ground of appeal of the revenue is hereby dismissed.

54.1 The TP issues raised by the Revenue have already been adjudicated along with the appeal of assessee vide paragraph number 47 of this order, wherein the grounds of appeal of the revenue were dismissed. For the detailed discussion, please refer the relevant paragraph. Hence, the grounds of appeal of the revenue are hereby dismissed.

55. In the result, the appeal of the Revenue is hereby dismissed.

56. In the combined result, the appeal of the assessee is hereby partly allowed for statistical purposes whereas the appeal of the revenue is hereby dismissed.

Order pronounced in court on 9th day of December, 2024