Addition of bogus LTCG u/s 68 deleted to prevent double taxation: ITAT Pune in Tamil

- Tamil Tax upate News

- March 16, 2025

- No Comment

- 67

- 110 minutes read

Ashok Vijaykumar Kotecha Vs ACIT (ITAT Pune)

In the case of Ashok Vijaykumar Kotecha vs. ACIT, Circle-1, Jalgaon (ITA No. 1453/PUN/2023), the Income Tax Appellate Tribunal (ITAT) Pune ruled in favor of the assessee, deleting the addition of ₹1.52 crore made under Section 68 of the Income Tax Act, 1961.

Case Background

The assessee, Ashok Vijaykumar Kotecha, filed his return for AY 2011-12, declaring an income of ₹1.79 crore. The assessment was originally completed under Section 143(3) read with Section 153A. However, the case was reopened under Section 147 after the Department received information from the investigation wing regarding transactions in the penny stock M/s Nivyah Infrastructure & Telecom Services Ltd.

The Assessing Officer (AO) alleged that the assessee had engaged in the sale of 78,925 shares of the said company for ₹1.52 crore, claiming tax exemption on Long-Term Capital Gains (LTCG) under Section 10(38). The AO concluded that the transactions were bogus, treating the proceeds as unexplained income under Section 68 and also adding ₹9.15 lakh under Section 69C as commission allegedly paid for entry facilitation.

Appeal and Tribunal Ruling

The key arguments before the ITAT included:

1. Double Taxation: The same amount had already been added to the income of Dilip Kotecha, the assessee’s brother, from whose premises the relevant documents were seized.

2. No Unexplained Income: The shares were allotted through a preferential issue, held in a demat account, and sold via recognized stock exchanges with applicable Securities Transaction Tax (STT).

3. No Independent Inquiry by AO: The addition was made solely based on third-party information without verifying the facts independently.

The Tribunal observed that:

- The sale proceeds of the shares were already taxed in the hands of Dilip Kotecha, whose appeal was dismissed, making any further addition in Ashok Kotecha’s hands a case of double taxation.

- Since the income had already suffered tax, the addition of ₹1.52 crore was unwarranted and was directed to be deleted.

- Consequently, the ₹9.15 lakh addition under Section 69C was also deleted.

Key Takeaways

1. Double taxation is impermissible: If an income has been assessed in one taxpayer’s hands, it cannot be assessed again in another’s without justifiable reason.

2. Mere suspicion is not sufficient: The AO must conduct independent inquiries before making additions under Section 68.

3. Penny stock transactions require due diligence: While tax authorities are cautious about penny stock manipulations, they must distinguish between genuine and bogus transactions.

This ruling reinforces the principle that taxpayers cannot be penalized merely based on assumptions, and proper verification is essential before invoking anti-abuse provisions like Section 68.

The case was represented by CA Kishor Phadke (Assisted by CA Saurabh Jadhav)

FULL TEXT OF THE ORDER OF ITAT PUNE

This appeal filed by the assessee is directed against the order dated 31.10.2023 of the Ld. CIT(A) / NFAC, Delhi relating to assessment year 2011-12.

2. Facts of the case, in brief, are that the assessee is an individual and director of a company. He derives income from ‘salary’ and ‘income from other sources’ and filed his return of income on 07.07.2013 declaring total income of Rs.1,79,42,630/- after claiming the deduction of Rs.1,15,000/- under Chapter VIA. An order u/s 143(3) r.w.s. 153A of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) was passed on 29.03.2014 accepting the income so declared. Subsequently, the Assessing Officer reopened the assessment u/s 147 of the Act after recording the following reasons:

“ORDER SHEET

| Name of the Assessee | Shri Ashok Vijay Kotecha |

| Address | 4, Teachers Colony, Opp. JDCC Bank, Ring Road, Jalgaon-425 001 |

| PAN | ABMPK41730 |

| Assessment Year (AY) | 2011-12 |

Reasons recorded for issue of notice u/s 148 of the I. T. Act, 1961

The assessee filed return of income for A.Y. 2011-12 on 07.07.2013 declaring total income at Rs.1,79,42,633/-. Order u/s 143(3) r.w.s. 153A passed with assessed income at Rs.1,79,42,633/- dated 29.03.2014. The assessee is director in Company and is showing income from salary and other source.

2. Information has also been received from DDIT(Inv) Unit 8(3), Mumbai showing that the assessee Shri Ashok Vijay Kotecha has traded with M/s Nivyah Infrastructure & Telecom Services Ltd which is a penny stock company listed on BSE with total Trade value Rs.1,52,62,200/- in F.Y. 2010-11 i.e. A.Y.2011-12. The Dy DIT(Inv) Unit 8(3) Mumbai vide its letter dated 23.03.2018 has stated as under:

“……Reliable information is received that M/s. Nivyah Infrastructure & Telecom Services Ltd. is a penny stock listed on BSE with Script Code (517534) and this company has been used to facilitate introduction of unaccounted income of members of beneficiaries in the form of exempt capital gain or Short Term Capital Loss in their books of accounts. It was noticed that share price of M/s. Nivyah Infrastructure & Telecom Services Ltd rose from Rs.39 on 2nd July 2009 to Rs.2050 on 5th Jan 2011and dipped to Rs.47.20 on 15th July 2012.

However, the financials of the company for the relevant period do not show any substantial change so as to support such as huge share price movement. The company does not have business worthwhile to justify the sharp rise in market price of shares. The sharp rise in the market price of this entity is not supported by financial fundamentals of the company. Both purchase and sale of the shares are concentrated within few persons/entities. The exit providers do not have creditworthiness. They are either non-filers or have filed nominal return of income and have not paid tax.

3. Subsequently, trade data of M/s. Nivyah Infrastructure & Telecom Services Ltd was called for from BSE and analysed. Following beneficiaries who have traded in this script during financial year 2010-11, pertains to your charge/jurisdiction.

| S.No. | PAN of the beneficiaries | Total Trade value for F.Y. 2010-11 (Inv Rs.) |

| 1 | ABMPK4173D | 15262200 |

………………………………………………………………”

In view of the above facts & circumstances the amount of Rs.1,52,62,200/- representing Trade value between the assessee and the penny stock company M/s Nivyah Infrastructure & Telecom Services Ltd has escaped assessment as the assessee had failed to disclose fully & truly all material facts necessary relating to the issue for her assessment for A.Y.2011-12.

5. Hence there is an under assessment of income and the assessment needs to be reopened u/s 147 by issue of notice u/s 148. Thus I have reason to believe that income to the tune of Rs.1,52,62,200 which is chargeable to tax for A.Y.2011-12 has escaped assessment in the hands of the assesses and it is a fit case for issue of notice u/s 148 for reopening the assessment u/s 147 of the Act.

6. In this case a return of income was filed for the year under consideration and regular assessment u/s 153A r.w.s. 143(3) was made on 29.03.2014. Since, 4 years from the end of the relevant year has expired in this case, the requirements to initiate proceeding u/s 147 of the Act are reason to believe that income for the year under consideration has escaped assessment because of failure on the part of the assessee to disclose fully and truly all material facts necessary for his assessment for the assessment year under consideration. It is pertinent to mention here that reason to believe that income has escaped assessment for the year under consideration have been recorded as mentioned above. I have carefully considered the assessment records containing the submissions made by the assessee in response to various notices issued during the assessment/re-assessment proceedings and have noted that the assessee has not fully and truly disclosed the following material facts necessary for his assessment for the year under consideration:-

1. The said amount of Rs.1,52,62,200/- being the trade value between the assessee and the penny stock company.

It is evident from the above facts that the assessee had not truly and fully disclosed material facts necessary for his assessment for the year under consideration thereby necessitating reopening u/s 147 of the Act.

It is true that the assessee has filed a copy of computation of income, P&L A/c and balance sheet alongwith return of income where various information /material were disclosed. However, the requisite full and true disclosure of all material facts necessary for assessment has not been made as noted above. It is pertinent to mention here that even though the assessee has produced computation of income, P&L A/c and balance sheet or other evidence as mentioned above, the requisite material facts as noted above in the reasons for reopening were embedded in such a manner that material evidence could not be discovered by the AO and could have been discovered with due diligence, accordingly attracting provisions of Explanation 1 of section 147 of the Act.

It is evident from the above discussion that in this case, the issues under consideration were never examined by the AO during the course of regular assessment / reassessment. This fact is corroborated from the contents of notices issued by the AO u/s 143(2)/142(1) and order sheet entries with various dates recorded during the 153A r.w.s. 143(3) proceedings. It is important to highlight here that material facts relevant for the assessment on the issue(s) under consideration were not filed during the course of assessment proceeding and the same may be embedded in audited P&L A/c, balance sheet and books of account in such a manner that it would require due diligence by the AO to exact these Information. For aforestated reasons, it is not a case of change of opinion by the AO.

In this case more than four years have lapsed from the end of assessment year under consideration. Hence necessary sanction to issue notice u/s 148 has been obtained separately from Principal Commissioner of Income Tax as per the provisions of section 151 of the Act.

In view of the above facts and circumstances, I have, therefore, reason to believe that the income chargeable to tax to the extent of Rs.1,52,62,200/- has escaped assessment for the relevant assessment year within the meaning of Explanation 2(c) to section 147 of the Income Tax Act, 1961.

Thus, notice u/s 148 of Income Tax Act, 1961 is issued after taking prior approval of competent authority.

Sd/-

ACIT, Central Circle-1, Nashik”

Date: 31/03/2018

3. In response to the same, the assessee filed the return of income on 06.12.2018 declaring total income of Rs.1,79,42,630/-. The objections raised by the assessee for reopening of the assessment were duly disposed of by the Assessing Officer vide order dated 14.09.2018 and subsequently again on 12.11.2018 after filing the second objection by the assessee. Thereafter, the Assessing Officer issued the statutory notices u/s 143(2) and 142(1) of the Act. The assessee in response to the said notices filed the requisite details from time to time.

4. During the course of assessment proceedings the Assessing Officer noted that the assessee has sold 78925 shares of M/s Nivyah Infrastructure & Telecom Services Ltd. (then known as M/s S.V. Electricals Ltd.) (Scrip ID:INE303D01022; Scrip Code:517534) in the month of January, 2011 for a total consideration of Rs.1,52,62,200/-. This is a listed security. The shares were sold after holding it for more than 12 months. STT was paid on the sale transaction. Accordingly, LTCG income was claimed as exempt u/s 10(38) of the IT Act, 1961. The shares of Nivyah Infrastructure & Telecom Services Ltd. (hereby referred to as “NITSL”) were allotted to the assessee via preferential mode of allotment directly from the company. 78925 preference shares of NITSL @ Rs. 12/- share were allotted to him from 01.04.2008 to 01.03.2010 through the preferential mode of allotment, for which the payment of Rs.9,47,100/- was made by the assessee. These 78925 shares were dematted through the assessee’s demat account held with Religare Securities Limited and were appearing as held by the assessee in his demat account as on 01.03.2010 and the shares were sold through the said broker with whom the assessee had trading accounts. Receipts from the sale of shares were credited to the assessee’s bank account by broker. The Assessing Officer summarized the details which are as under:

| No. of shares | Purchase price | Total cost of acquisition | Sale price | Total sales consideration | LTCG income |

| 78925 | Re.12/- share (pref. allotment) |

Rs.9,47,100/- | Rs.193.37/- share | Rs.15262200/- | — |

5. He, therefore, asked the assessee to explain as to why the bogus long term capital of Rs.1,52,62,200/- should not be added to his total income u/s 68 of the Act. Rejecting the various explanations given by the assessee and observing that the assessee purchased the shares of M/s. S.V. Electricals Ltd. / NITSL with the sole intention of earning profit from the penny stock and therefore, such transaction is clearly ‘adventure in the nature of trade’. He accordingly made addition of Rs.1,52,62,200/- u/s 68 of the Act treating the long term capital gain claimed as exempt by the assessee u/s 10(38) of the Act as bogus. The Assessing Officer further made addition of Rs.9,15,732/- u/s 69C of the Act being the commission paid in cash for arranging such accommodation entries which has not been recorded in the books of account. Thus, the Assessing Officer determined the total income of the assessee at Rs.3,41,20,562/-.

6. Before the Ld. CIT(A) / NFAC apart from challenging the addition on merit, challenged the validity of re-assessment proceedings. However, the Ld. CIT(A) / NFAC was also not satisfied with the arguments of the assessee and upheld the validity of re-assessment proceedings as well as the addition on merit.

7. Aggrieved with such order of the Ld. CIT(A) / NFAC, the assessee is in appeal before the Tribunal by raising the following grounds:

1. The CIT(A) NFAC (hereinafter called as learned CIT(A)) erred in law and on facts in upholding the addition made by learned AO u/s 68 and Section 69C of ITA, 1961 amounting to Rs.1,52,62,200 and Rs.9,15,732 respectively thereby confirming the assessed income to the tune of Rs.3,41,20,562/- as against the returned income of Rs.1,79,42,630/-

2. The learned CIT(A) erred in upholding the reassessment proceedings when admittedly conditions specified u/s 147 of the ITA, 1961 for valid initiation were not satisfied in as much as all the facts were truly and fully disclosed in the original assessment proceedings and order was passed after due verification. As such, the addition was only the result of a change in opinion and the action on the part of the learned AO was based upon the information stated to have been received from the Investigation wing and not on independent inquiry.

3. The learned CIT(A) NFAC and learned AO (hereinafter referred to as learned I-T authorities) failed to appreciate the facts that addition of Rs. 1,52,62,200 u/s 68 on account of bogus LTCG in the returned income of the appellant’s return income would lead to double addition as the Hon’ble ITAT Pune Bench has already upheld the addition in the hands of appellant’s brother w.r.t same share transaction pertaining to M/s S.V Electricals.

4. The learned I-T authorities erred in law and on facts in treating the transaction as a colorable device to evade taxes, merely because appellant’s share name i.e. M/s S.V Electricals was appearing in the Investigation Wing Kolkata Report. The learned I-T authorities ought to have appreciated that there is no evidence that the appellant has obtained bogus long-term capital gain exemption from the sale of shares of M/s S.V Electricals.

5. The learned I-T authorities erred in law and facts in making addition of Rs.9,15,732 (6% of LTCG) being alleged commission paid to entry providers on an ad-hoc basis.

6. The learned AO erred in law and facts in passing the impugned order without issuing show cause notice which is a mandatory pre-requisite as per CBDT circular. The learned CIT(A) failed to appreciate the fact that the notice dated 06/12/2018 as mentioned in the assessment order is a notice u/s 142(1) / 143(2) and not a show cause notice.

7. Appellant craves leave to add/ alter/delete/modify, all/ any of the above grounds of appeal.

8. Although the assessee has raised so many grounds, however, the Ld. Counsel for the assessee confined his argument to the addition of Rs.1,52,62,000/-made by the Assessing Officer u/s 68 of the Act and addition of Rs.9,15,732/-being the alleged commission paid to entry providers being 6% of such long term capital gain on adhoc basis. The Ld. Counsel for the assessee filed the following chart:

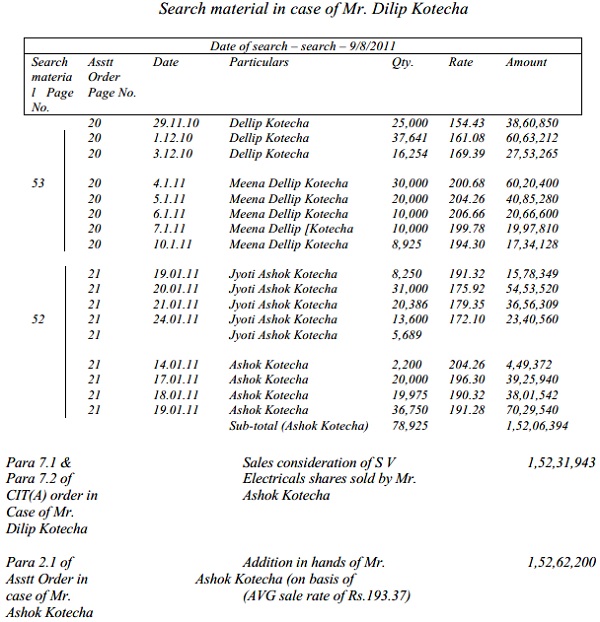

Search material in case of Mr. Dilip Kotecha

9. Referring to para 2.1 of the assessment order in case of Ashok Vijaykumar Kotecha i.e. the assessee, he drew the attention of the Bench to the same which reads as under:

“2.1 During FY 2010-11, the assessee sold 78925 shares of M/s Nivyah Infrastructure & Telecom Services Ltd. (then known as M/s S.V. Electricals Ltd.) (Scrip ID:INE303D01022; Scrip Code:517534) in the month of January, 2011 for total consideration of Rs.1,52,62,200/-. This is a listed security.Shares were sold after holding it for more than 12 months. STT was paid on the sale transaction Accordingly, LTCG income was claimed as exempt u/s 10(38) of the IT Act, 1961.”

10. Referring to para 7.1 of the order of Ld. CIT(A) / NFAC in the case of Shri Dilip Kotecha, brother of the assessee from whose residence the details were found during the course of survey, he drew the attention of the Bench to the same which reads as under:

“7.1 The appellant vide submission dated nil contended as under:

a) “The Assessing Officer has wrongly added Rs.6,20,00,000/- by way of investment out of undisclosed sources.

b) The Assessing Officer has referred to page no. 62 of seized material Annexure A5. The Assessing Officer has noted that in the said paper there is a working of transactions of sale of shares of M/s S.V. Electricals. The Assessing Officer has contended that Rs.7,88,400/-was paid by cheque and balance of Rs.6,18,70,371/- was to be paid in cash. The Assessing Officer has observed that the Appellant has paid cash amounting to Rs.6.20,00,000/- to the person who is alleged to have made the noting. In this regard, it was duly explained to the Assessing Officer that the said page was only a rough calculation of the transaction. The Appellant denied having made any cash payment of Rs.6,20,00,000/-. It was further submitted that the said transactions have already materialized and entered in the hooks of accounts. It was therefore submitted that the question of further addition of Rs.6,20,00,000/- does not arise. However, the Assessing Officer added the same by rejecting the explanation of the appellant. It is worth to mention that the transaction is of sale of shares and the assessee had to receive the payment, which he received by cheque only. The question of receiving the payment over and above the sale price does not arises as the sales of shares were done at recognized stock exchange on BOLT [i.e. Online Trading System). The rates are as per the quotation of a particular day as the transactions are of listed equity shares.

c) The said addition is not tenable as follows:

i) The transactions of sale of shares amounting to Rs.6,26,58,771/- are duly accounted for in the respective books of the family members of the Appellant. Therefore, the same amounts to addition of the sums already reflected in the books of accounts.

| Date | Name | Amount (Rs.) |

| 19.01.2011 to 25.03.2011 | Jyoti Ashok Kotecha | 1,35,49,484/- |

| 14.01.2011 to 19.01.2011 | Ashok Vijaykumar Kotecha | 1,52,31.943/- |

| 04.01.2011 to 10.01.2011 | Meena Dellip Kotecha | 1,59,29,594/- |

| 01.12.2010 to

03.12.2010 |

Dellip Vijaykumar Kotecha | 1,27,01,823/- |

(ii) Since the respective family members have already accounted for respective sales proceeds of sale of shares, the addition made by the Assessing Officer in the hands of the Appellant is uncalled for.

iii) The Assessing Officer has merely added Rs.6,20,00,000/- only on the basis of relevant loose paper without verifying the same from other files.

iv) It was also pointed out to the Assessing Officer that the said paper is not in handwriting of the Appellant. Therefore, the Appellant is unable to comment further on the contents written by the alleged owner of the said paper.

v) The Assessing Officer has made the addition by way of undisclosed investment which is entirely erroneous because the respective family members have already entered the sale proceeds in their books. In the case of P.K.Noorjahan [237 ITR 570 (SC)], it is held that, “The submission is that the word ‘may’ in section 69 should be read as ‘shall”. We are unable to agree. As pointed out by the Tribunal, in the corresponding clause in the Bill which was introduced in the Parliament, the word ‘shall had been used but during the course of consideration of the Bill and on the recommendation of the Select Committee, the said word was substituted by the word ‘may. This clearly indicates that the intention of the Parliament in enacting section 69 was to confer a discretion on the ITO in the matter of treating the source of investment which has not been satisfactorily explained by the assessee as the income of the assessee and the ITO is not obliged to treat such source of investment as income in every case where the explanation offered by the assessee is found to be not satisfactory. The question whether the source of the investment should be treated as income or not under section 69 has to be considered in the light of the facts of each case. In other words, a discretion has been conferred on the ITO under section 69 to treat the source of investment as the income of the assessee if the explanation offered by the assessee is not found satisfactory and the said discretion has to be exercised keeping in view the facts and circumstances of the particular case.

vi) In this case, the full amount of sales proceeds are fully accounted for as above said. Similarly, respective purchases are also accounted for in the books of accounts maintained. Therefore, there is no question of any undisclosed investment. Therefore, the same is bad in law and deserves to be deleted”

11. Referring to paras 7.2 to 7.5 of the order of the Ld. CIT(A) / NFAC in the case of Shri Dilip V. Kotecha, brother of the assessee, he drew the attention of the Bench to the same which read as under:

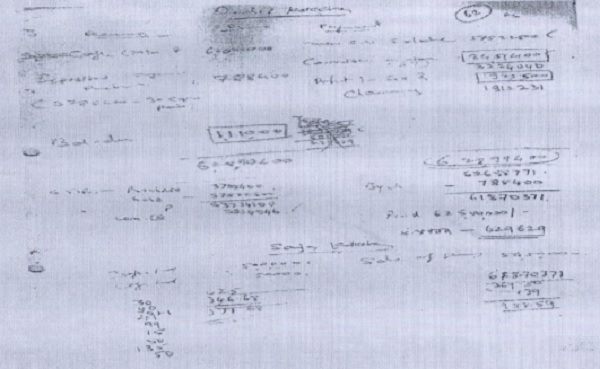

7.2 I have gone through the assessment order and the submissions filed by the appellant. Brief facts are that during the course of search at the residential premise of the appellant, one loose paper was seized at page No.62 of Annexure A-5 wherein certain transactions in the shares along with payment by cash and cheque were recorded. For better appreciation of facts, the scanned image of page 62 is reproduced below:

According to AO, the details were working of transactions related to sale of shares of M/s. S.V. Electricals. The shares were sold, the commission was paid and profit was booked and as per the working the paper, appellant had to make total payment of Rs.6,26,58,771/-. Appellant had paid amount of Rs.6,20,00,000 in cash to the person who had made notings. This cash transaction was not found recorded in the books of accounts and therefore same was added by the AO as undisclosed income of the appellant. On the other hand, appellant contended before the AO on that page there was only rough calculation of transaction and no cash payment except sundry amounts for delivery or D-Mat charges was paid. It was admitted that all the transactions in the shares were duly recorded in the books of accounts and no amount apart from what was recorded in the books was paid. However, AO did not accept the explanation in view of clear recording of cash payment of Rs.6,20,00,000.

7.3 During the course of appellate proceedings, appellant was asked to file details of share transactions in the scrip S.V. Electricals undertaken by the appellant or his family members during the year under consideration. Summarised details of the transactions, submitted by the appellant before the AO are reproduced below :

JYOTI ASHOKA KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V. ELECTRI CALS |

22-12-09 |

78925 |

947100.00 |

19.01.2011 |

8250 |

1580865 |

1481865 |

|

20.01.2011 |

31000 |

5461106 |

5089106 |

|||||

21.01.2011 |

20386 |

3662141 |

3417509 |

|||||

24.01.2011 |

13600 |

2348040 |

2184840 |

|||||

25.03.2011 |

5689 |

497333 |

429064 |

|||||

TOTAL |

78925 |

947100.00 |

78925 |

13549484.00 |

12602384.00 |

0.00 |

||

ASHOKA VIJAYKUMAR KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V.ELECTRI CALS |

22-12-09 |

78925 |

947100.00 |

14.01.2011 |

2200 |

450098 |

423698 |

|

17.01.2011 |

20000 |

3932200 |

3692200 |

|||||

18.01.2011 |

19975 |

3807610 |

3567910 |

|||||

19.01.2011 |

36750 |

7042035 |

6601035 |

|||||

TOTAL |

78925 |

947100.00 |

15231943.00 |

14284843.00 |

0.00 |

|||

MEENA DEELIP KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V.ELECTRI CALS |

19-12-09 |

78925 |

947100.00 |

04.01.2011 |

30000 |

6030000.00 |

5670000.00 |

|

07.01.2011 |

10000 |

2001000.00 |

1881000.00 |

|||||

07.01.2011 |

20000 |

4091800.00 |

3851800.00 |

|||||

10.01.2011 |

8925 |

1736894.25 |

1629794.25 |

|||||

10.03.2011 |

10000 |

2069900.00 |

1949900.00 |

|||||

TOTAL |

78925 |

947100.00 |

78925 |

15929594.25 |

14982494.25 |

0.00 |

||

DEELIP VIJAYKUMAR KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

| COMPAN Y NAME | PURCHASE | SOLD | DIFFERENCE | |||||

| DATE | QUNTY | AMOUNT | DATE | QUNTY | AMOUNT | PROFIT | LOSS | |

| S.V.

ELECTRI CALS |

09-10-09 | 78925 | 947100.00 | 01-12-10 | 37641 | 6072550.10 | 5620858.10 | |

| 01-12-10 | 25000 | 3866799.00 | 3566799.00 | |||||

| 03-12-10 | 16284 | 2762473.44 | 2567335.44 | |||||

| TOTAL | 78925 | 947100.00 | 78925 | 12701822.54 | 11754992.54 | 0.00 | ||

According to the summary, appellant in his own name and in the names of family members purchased shares of S.V. Electricals in the month of October, 2009 and December, 2009 respectively, Total purchase consideration paid by them is as under:

| Name | Date | Quantity | Amount (Rs.) |

Average Rate (Rs) per share |

| Dellip V. Kotecha | 9.10.2009 | 78,925 | 9,47,100 | 12 |

| Meena D Kotecha (appellant‘s wife) | 19.12.2009 | 78,925 | 9,47,100 | 12 |

| Ashok V. Kotecha (Appellant‘s brother) | 22.12.2009 | 78,925 | 9,47,100 | 12 |

| Jyoti A. Kotecha (appellant‘s brother‘s wife) | 19.12.2009 | 78,925 | 9,47,100 | 12 |

| TOTAL | 3,15,700 | 37,88,400 | 12 |

Similarly, details of sale of the shares can be summarized as under:

| Name | Date | Quantity | Amount (Rs) | Average

Rate (Rs) |

Profit earned |

| Dellip V. Kotecha (appellant) | 1.12.2010 & 3.12.2010 | 78,925 | 1,27,01,822.54 | 160.93 | 1,17,54,992 |

| Meena D Kotecha (appellant‘s wife) |

4.1.2010 to 10.1.2011 | 78,925 | 1,59,29,594.25 | 201.83 | 1,49,82,494 |

| Ashok V. Kotecha (Appellant‘s brother) |

14.1.2011 to 19.1.2011 | 78,925 | 1,52,31,943.00 | 192.99 | 1,42,84,843 |

| Jyoti A. Kotecha (appellant‘s brother‘s wife) | 19.1.2011 to 25.3.2011 | 78,925 | 1,35,49,484.00 | 171.67 | 1,26,02,384 |

| TOTAL | 3,15,700 | 5,74,12,843.79 | 181.85 | 5,36,24,713 |

As per appellant, all the members who have purchased and sold the shares of S.V. Electricals had disclosed the Long Term Capital Gain in their respective returns and also claimed exemption u/s 10(38) of the Act.

As per appellant, all the members who have purchased and sold the shares of S.V. Electricals had disclosed the Long Term Capital Gain in their respective returns and also claimed exemption u/s 10(38) of the Act.

7.4 In this background, the loose paper No.62 seized from the residential premise of the appellant has to be examined. The account prepared on the loose paper has been addressed to the appellant and revealed receipts on the left hand side and payments on the right hand side. On the payment side, the total was shown at Rs 5,75,22,500 against S.V. Electricals. Below that commission 6% of the sale proceeds of Rs 34,51,400 (below that revised amount of Rs 32,24,046) was mentioned. Below that some other charges of Rs 19,25,500 (below that revised amount of Rs 19,12,231) were mentioned. On the receipt side, cash amount of Rs 6.20.00.000 and below that deposit against purchase of Rs 7,88,400 was mentioned. Further, below purchase deposit the amount (37,88,400-30 cash paid) was written. Again the transaction has been summarized in the middle of the page showing total of S.V.E. purchase at Rs 37,88,400 and sale at Rs 5,75,22,500 with commission at Rs 32,24,046 has been mentioned. Against that cheque payment of Rs 7,88,400 was mentioned. As discussed in para 5.3 of this order, on the bottom of the page similar details in respect of Sanjay Kotecha were given. While explaining the entries pertaining to Sanjay Kotecha, appellant mentioned that papers were the working prepared by one Tejas Kawadia who was representative of M/s Religare Securities Ltd. and paper was inadvertently left by him at his premise. In respect of transaction summarized in the name of appellant, it was stated that all the transactions related to sales of S.V. Electricals were recorded in the books of accounts of respective family members Only transactions mentioned through cheque were claimed to be correct and payment recorded in cash were denied. This is a classic case where entire account pertaining to accommodation entry for purchasing long term capital gains was found recorded on the seized paper. But for this paper, appellant and other family members have claimed long term capital gains in their respective returns as genuine. 5.V. Electricals is a typical penny stock as its value appreciated from Rs 12 per share in December, 2009 to Rs 200 per share in January 2011 1.e., appreciation in value of about 1600 in the period of 13 months. There are no supporting financial of 5.V. Electricals to justify dramatic rise in the value of shares. As the summary prepared above revealed that for purpose of purchasing accommodation entries of the long term capital gains, the appellant purchased 3,15,700 shares in name of 4 persons @ Rs 12 per share and the payment of Rs 37,88,400 was made by way of cheque. Since transaction was sham, after the cheques were issued for purchase of shares of Rs 37,88,400 the appellant was paid cash of Rs 30,00,000 back as found recorded in the loose paper. In this manner, the operator only had amount of Rs 7,88,400 (37,88,400-30,00,000) with him which was mentioned as deposit with him against the purchase and also shown as amount received through cheque. Later on sales of shares the operator recorded sale proceeds which was given through cheque at Rs 5,75,22,500. For purchasing the accommodation entries, the operator charged commission of Rs 32,24,046 and also other expenses and D-mat charges, at Rs 19.12.231. In this manner, operator had to receive back the cash difference on account of cheque issued on sale of shares along with his commission and other charges. Accordingly, the operator had received cash of Rs 6.20,00,000 from the appellant. All the transactions are written in detail and the cheque portion matched with the books of accounts of the appellant and other family members. Therefore, denial by the appellant that it was a genuine transaction and no cash was paid is not credible. The appellant had partly admitted the transactions recorded on the loose paper as true but denied the cash transaction to save his skin. As per presumption u/s 292C rws 132(4A) of the Act, all the transactions found recorded on the seized papers are to be treated as true and genuine. Without any corroborative evidences, simple denial by the appellant regarding correctness of the recorded transactions would not rebut the presumption. It is therefore held that appellant has purchased long term capital gain in his name and in name of other family members from accommodation entry provider in the transactions of penny stock S.V. Electricals, Appellant had paid Rs 6,20,00,000 in cash to get exempt long term capital gains of Rs 5,36,24,713 in his name and in name of other family members. Money was paid by the appellant therefore, I uphold the addition of Rs 6,20,00,000 being undisclosed income of the appellant for the year under consideration. Ground raised by the appellant is dismissed.

7.5 During the course of appellate proceedings, appellant without prejudice to denying the cash transaction, submitted that separate additions were made for cash loan advanced of Rs 1,38,38.000 and cash given of Rs 6,20,00,000 on account of payment in connection with long term capital gains. Appellant sought telescoping of cash advance given against the addition made of Rs 6,20,00,000. I have considered the request but do not find any merit in it as on the loose paper where cash loan transactions were recorded, cash received was on 25.1.2011 and 19.1.2011. There is no date against the payment of Rs 6,20,00,000 made by the appellant to the entry operator. Therefore, it cannot be said that amount received back from the borrower was used for purchasing the long term capital gains. No telescopic benefit can therefore be granted to him.”

12. Referring to the above, he submitted that the Ld. CIT(A) / NFAC has given a finding that the assessee has purchased long term capital in his name and in name of other family members from accommodation entry provider in the transactions of penny stock S.V. Electricals for which he had paid Rs.6,20,00,000 in cash to get exempt long term capital gains of Rs.5,36,24,713/- in his name and in name of other family members.

13. He submitted that the seized documents were found from the premises of Shri Dilip Kotecha and addition has already been made by the Assessing Officer in his case in respect to the transaction of shares of Ashok Vijaykumar Kotecha which has been upheld by the Ld. CIT(A) / NFAC. Referring to the decision of the Pune Bench of the Tribunal in the case of Shri Dilip Kotecha vide ITA No.203/PUN/2016, order dated 25.04.2022 for assessment year 2011-12, he submitted that the Tribunal has upheld the order of the Ld. CIT(A) and dismissed the appeal of Shri Dilip Kotecha. Thus, once the amount of Rs.1,52,62,200/- has already been added in the hands of Shri Dilip Kotecha which has attained finality, addition of the same in the hands of the assessee i.e. Ashok Vijaykumar Kotecha will amount to double addition and therefore, the same should be deleted.

14. The Ld. DR on the other hand while supporting the orders of the Assessing Officer and the Ld. CIT(A) / NFAC filed the comments of the Assessing Officer on this issue raised by the Ld. Counsel for the assessee which read as under:

“To,

The Jt. Commissioner of Income Tax.

ITAT-1, Pune.

Sir,

Sub:- Forwarding of comments on ground of appeal in the case of Shri Ashok V. Kotecha, ITA No.1453/PUN/2023, for A. Y. 2011-12-reg

Ref: Your office Letter No.PN/JH.CIT/AVK/2024-25/275, date: 10.07.2024. Kindly refer to the above.

02 This office has received the above mentioned letter seeking comments on Grounds of appeal No.03 in the case of Shri Ahsok V. Kotecha, in appeal No. ITA No.1453/PUN/2023, for A.Y. 2011-12.

03. After perusal of the particular Ground of assessee it is submitted that, the assessee has mentioned that (in ground no.03), the addition of Rs. 1,52,62,200/- u/s 68 on account of bogus LTCG would lead to double addition as the Hon’ble ITAT Pune Bench has already upheld the addition in the hands of assessee’s brother (Shri Dilip Kotecha) w.r.t same share transaction pertaining to M/s S.V. Electricals.

04. In the case of Shri Ashok V. Kotecha, the assessment order passed by the then AO dated: 28.12.2018 u/s 147 r.w.s. 143(3) of the Act clearly indicates that the addition of Rs.1,52,62,200/- was made on account of bogus LTCG claim u/s 68 of the Act, which was held as the profit from the sale of shares of S.V. Electricals/NITSL. The then AO in his assessment order held that, the assessee sold 78925 shares of M/s Nivyah Infrastructure & Telecom Services Ltd. (then known as S.V. Electricals Ltd.) in the month of January, 2011 for total consideration of Rs.1,52,62,200/-.

05. Whereas in the case of Shri Dilip V. Kotecha, the assessment order was passed by the then AO on 28.12.2018 u/s 143(3) r.w.s. 147 of the Act assessing the total income at Rs.9,65,49,046/-.

06. In the assessment order passed u/s 143(3) r.w.s 153A of the Act the then AO has held that the assessee Shri Dilip V. Kotecha, has offered sum of Rs.7,00,00,000/- as additional income in his return of Income for Tax as a result of the search declaring it to be (undisclosed) investment offered for tax during the search. It is pertinent to mention here that a search in the “Kotecha” group of cases was conducted on 09.08.2011. During the course of search action at the assessee’s residence, some loose papers were found in which at page No.62 contained the hand written noting made in pen, under the head ‘Deelip Kotecha‘ and „Sanjay Kotecha‘. The noting under the head ‘Deelip Kotecha’ was a working of the transaction of sale of shares of M/s S.V. Electricals. These shares have been noted to have been sold, commission paid and profit booked. The some total of all the noting was that Shri Dilip Kotecha has to make a payment of Rs.6,26,58,771/-. Out of this amount sum of Rs.7,88,400/- was paid by cheque, balance of Rs.6,18,70,371/- was to be paid in cash against which the assessee paid sum of Rs.6,25,00,000/-.

07. After perusing the assessment order’s and observing the facts of the cases of both Shri Ashok V. Kotecha and Shri Dilip V. Kotecha for A.Y. 2011-12 it is observed that the addition made in the case of Shri Dilip V. Kotecha for said A.Y was based on the evidences seized/found from the premises/residences of the assessee.

08. Whereas, the addition made in the case of Shri Ashok V. Kotecha for A.Y. 2011-12 was on account of bogus LTCG claim u/s 68 of the Act which was related solely to the assessee Shri Ashok V. Kotecha.

09. In view of all the facts mentioned and described above, it is submitted that the claim of the assesseee stated in your office letter referenced above, that the “addition of Rs.1,52,62,200/- u/s 68 on account of bogus LTCG in the returned income of the appellant’s return income would lead to double addition” is found to be incorrect. The assessment orders in both the cases are enclosed with this letter for reference.

Submitted.

Yours Faithfully

Sd/-

(S.R. BODHARE)

Assistant Commissioner of Income Tax

Circle -1, Jalgaon

Enclosure:-As above”

15. He accordingly submitted that the order of the Ld. CIT(A) / NFAC be upheld and the grounds raised by the assessee be dismissed.

16. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the Assessing Officer in the instant case in the order passed u/s 143(3) r.w.s. 147 of the Act dated 28.12.2018 made the addition of Rs.1,52,62,200/- u/s 68 of the Act being the long term capital gain claimed as exempt u/s 10(38) of the Act by the assessee on account of sale of 78925 shares of M/s Nivyah Infrastructure & Telecom Services Ltd. While doing so, he held that bell-shaped pattern of the movement of share price is typical of a penny stock where the prices have been artificially rigged. The price of the shares in absence of any underlying fundamentals and drivers of growth, seem beyond the realm of any probability. It is his observation that the whole transaction was set up to earn profit from the penny stock and therefore, the transaction is clearly in the nature of adventure in trade. The Assessing Officer accordingly invoked the provisions of section 68 of the Act for making addition of Rs. 1,52,62,200/-. Similarly, the Assessing Officer also made addition of Rs.9,47,100/- being the estimated commission paid for arranging such accommodation entries. We find the Ld. CIT(A) / NFAC upheld the action of the Assessing Officer and also dismissed the grounds raised by the assessee challenging the validity of re-assessment proceedings.

17. It is the submission of the Ld. Counsel for the assessee that the details of transaction in the shares of M/s Nivyah Infrastructure & Telecom Services Ltd. were found from the premises of the brother of assessee Shri Dilip V Kotecha and the Assessing Officer has made addition of the same in the hands of Mr. Dilip Kotecha despite his argument that various family members have disclosed their respective profit in their returns of income. We find despite arguing before the Ld. CIT(A) / NFAC that various family members have disclosed their respective incomes from trading in the shares of M/s. Nivyah Infrastructure & Telecom Services Ltd., he rejected the same and upheld the order of the Assessing Officer. We find on further appeal by the assessee, the Tribunal has confirmed the order of the Ld. CIT(A) / NFAC. Therefore, we find merit in the argument of Ld. Counsel for the assessee that the addition in the hands of the assessee on account of profit on sale of same shares will amount to double addition which is not in accordance with law.

18. A perusal of para 2.1 of the assessment order which has been reproduced in the preceding paragraphs shows that the assessee sold 78925 shares of M/s Nivyah Infrastructure & Telecom Services Ltd. for a consideration of Rs.1,52,62,200/-. A perusal of the order of the Ld. CIT(A) / NFAC in the case of Shri Dilip V. Kotecha, copy of which has been filed in the paper book at pages 72 to 107 shows that during the appeal proceedings, he had given a breakup of the transaction of sale of shares amounting to Rs.6,26,58,771/- in the hands of four family members, the details of which are as under:

| Date | Name | Amount (Rs.) |

| 19.01.2011 to 25.03.2011 | Jyoti Ashok Kotecha | 1,35,49,484/- |

| 14.01.2011 to 19.01.2011 | Ashok Vijaykumar Kotecha | 1,52,31.943/- |

| 04.01.2011 to 10.01.2011 | Meena Dellip Kotecha | 1,59,29,594/- |

| 01.12.2010 to 03.12.2010 | Dellip Vijaykumar Kotecha | 1,27,01,823/- |

19. We find again on being asked by the Ld. CIT(A) / NFAC, the assessee had filed the details of share transactions in the scrip S.V. Electricals undertaken by the family members which were filed before the Assessing Officer and the Ld. CIT(A)/ NFAC in the case of Shri Dilip Vijaykumar Kotecha, the details of which are as under:

JYOTI ASHOKA KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V. ELECTRI CALS |

22-12-09 |

78925 |

947100.00 |

19.01.2011 |

8250 |

1580865 |

1481865 |

|

20.01.2011 |

31000 |

5461106 |

5089106 |

|||||

21.01.2011 |

20386 |

3662141 |

3417509 |

|||||

24.01.2011 |

13600 |

2348040 |

2184840 |

|||||

25.03.2011 |

5689 |

497333 |

429064 |

|||||

TOTAL |

78925 |

947100.00 |

78925 |

13549484.00 |

12602384.00 |

0.00 |

||

ASHOKA VIJAYKUMAR KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V.ELECTRI CALS |

22-12-09 |

78925 |

947100.00 |

14.01.2011 |

2200 |

450098 |

423698 |

|

17.01.2011 |

20000 |

3932200 |

3692200 |

|||||

18.01.2011 |

19975 |

3807610 |

3567910 |

|||||

19.01.2011 |

36750 |

7042035 |

6601035 |

|||||

TOTAL |

78925 |

947100.00 |

15231943.00 |

14284843.00 |

0.00 |

|||

MEENA DEELIP KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V.ELECTRI CALS |

19-12-09 |

78925 |

947100.00 |

04.01.2011 |

30000 |

6030000.00 |

5670000.00 |

|

07.01.2011 |

10000 |

2001000.00 |

1881000.00 |

|||||

07.01.2011 |

20000 |

4091800.00 |

3851800.00 |

|||||

10.01.2011 |

8925 |

1736894.25 |

1629794.25 |

|||||

10.03.2011 |

10000 |

2069900.00 |

1949900.00 |

|||||

TOTAL |

78925 |

947100.00 |

78925 |

15929594.25 |

14982494.25 |

0.00 |

||

DEELIP VIJAYKUMAR KOTECHA

SHARES LONG TERM PROFIT AS ON 31-03-11

COMPAN Y NAME |

PURCHASE |

SOLD |

DIFFERENCE |

|||||

DATE |

QUNTY |

AMOUNT |

DATE |

QUNTY |

AMOUNT |

PROFIT |

LOSS |

|

S.V.ELECTRI CALS |

09-10-09 |

78925 |

947100.00 |

01-12-10 |

37641 |

6072550.10 |

5620858.10 |

|

01-12-10 |

25000 |

3866799.00 |

3566799.00 |

|||||

03-12-10 |

16284 |

2762473.44 |

2567335.44 |

|||||

TOTAL |

78925 |

947100.00 |

78925 |

12701822.54 |

11754992.54 |

0.00 |

||

According to the summary, appellant in his own name and in the names of family members purchased shares of S.V. Electricals in the month of October, 2009 and December, 2009 respectively, Total purchase consideration paid by them is as under:

| Name | Date | Quantity | Amount (Rs.) |

Average Rate (Rs) per share |

| Dellip V. Kotecha | 9.10.2009 | 78,925 | 9,47,100 | 12 |

| Meena D Kotecha (appellant‘s wife) | 19.12.2009 | 78,925 | 9,47,100 | 12 |

| Ashok V. Kotecha (Appellant‘s brother) |

22.12.2009 | 78,925 | 9,47,100 | 12 |

| Jyoti A. Kotecha (appellant‘s brother‘s wife) | 19.12.2009 | 78,925 | 9,47,100 | 12 |

| TOTAL | 3,15,700 | 37,88,400 | 12 |

Similarly, details of sale of the shares can be summarized as under:

| Name | Date | Quantity | Amount (Rs) | Average Rate (Rs) per share | Profit earned |

| Dellip V. Kotecha (appellant) | 1.12.2010 & 3.12.2010 | 78,925 | 1,27,01,822.54 | 160.93 | 1,17,54,992 |

| Meena D Kotecha (appellant‘s wife) |

4.1.2010 to 10.1.2011 | 78,925 | 1,59,29,594.25 | 201.83 | 1,49,82,494 |

| Ashok V. Kotecha (Appellant‘s brother) |

14.1.2011 to 19.1.2011 | 78,925 | 1,52,31,943.00 | 192.99 | 1,42,84,843 |

| Jyoti A. Kotecha

(appellant‘s brother‘s wife) |

19.1.2011 to 25.3.2011 | 78,925 | 1,35,49,484.00 | 171.67 | 1,26,02,384 |

| TOTAL | 3,15,700 | 5,74,12,843.79 | 181.85 | 5,36,24,713 |

20. We find after considering the details the Ld. CIT(A) / NFAC had confirmed the addition of Rs.6,20,00,000/- in the hands of Shri Dilip Vijaykumar Kotecha as his undisclosed income. We find when Shri Dilip V. Kotecha challenged the order of the Ld. CIT(A) / NFAC before the Tribunal, the Tribunal vide ITA No.203/PUN/2016 order dated 25.04.2022 upheld the action of the Ld. CIT(A) by observing as under:

“11. We heard the rival submissions and perused the material on record.

As regards to the addition of Rs.1,38,38,000/-, the ld. AR submitted that the impugned addition was made based on the loose papers found and seized from the residential premises of the appellant as a result of search and seizure operations. We have carefully gone through the said loose documents which is also extracted by the Assessing Officer vide para no.8 of the assessment order, wherein, the documents dated 31.01.2011 indicates total payment of Rs.1,38,38,000/-. Obviously contents of the notings clearly indicate the payment of interest which means the appellant either repaid the loan with interest or made advance of loan for interest. Notings found therein represents the unexplained income out of which the loan or advance was made warranting addition under the provisions of section 69 of the Act. When this information/material was confronted to the appellant, the appellant had failed to explain the contents of the documents. Therefore, the Assessing Officer was justified in making the addition. Thus, we confirm the addition of Rs.1,38,38,000/-. Thus, the ground of appeal no.2 raised by the appellant stands dismissed.

Similarly, as regards to the addition of Rs.6,20,00,000/-, the ld. AR submitted that this addition is based on the contents of page no.62 found and seized during the course of search and seizure operations marked as Annexure-A/5. We have carefully gone through the said page which is placed at page no.33 of the Paper Book, which clearly indicates the receipts and payments made in connection with the purchase and sale of share of M/s S.V. Electricals and it reflects the name of Shri Deelip V. Kotecha, the appellant before us, had paid cash of Rs.6,20,00,000/- to the agent involving in booking of accommodations entries. The ld. CIT(A) had clearly narrated the transaction that would have taken place the findings recorded by CIT(A) remains uncontroverted by the appellant. When this matter was confronted to the appellant, he gave vague answers and, therefore, presumption created u/s 132(4A) remains un-rebutted. In the circumstances, the lower authorities were justified in making the addition as undisclosed investments u/s 69 of the Act. Thus, the ground of appeal no.3 raised by the appellant stand dismissed.”

21. Thus, it is crystal clear from the evidences placed before us which were also available with the lower authorities that the amount of Rs.1,52,06,394/- has already been suffered to tax in the hands of the brother of assessee Shri Dilip Vijaykumar Kotecha from whose premises the details of such sale of shares of M/s Nivyah Infrastructure & Telecom Services Ltd. were found. Under these circumstances, we find merit in the arguments of the Ld. Counsel for the assessee that the addition of amount of Rs.1,52,06,394/- in the hands of the assessee again will amount to double addition of the same i.e. once in the hands of the brother of the assessee and again in the hands of the assessee himself. Since this amount of Rs.1,52,06,394/-has already suffered to tax in the hands of Shri Dilip Vijaykumar Kotecha which has attained finality, therefore, we set aside the order of the Ld. CIT(A) / NFAC on this issue and direct the Assessing Officer to delete the addition. The ground raised by the assessee challenging the addition of Rs.1,52,06,394/- is accordingly allowed.

22. Since the addition of Rs.1,52,06,394/- is deleted, the order of the Ld. CIT(A)/ NFAC confirming the addition of Rs.9,15,732/- being the amount of commission paid for arranging such accommodation entries has no legs to stand. Accordingly, the same is also directed to be deleted. Since the Ld. Counsel for the assessee did not argue the grounds challenging the validity of re-assessment proceedings, the same are dismissed as ‘not pressed’.

23. In the result, the appeal filed by the assessee is partly allowed. Order pronounced in the open Court on 24th February, 2025.